Dr. Debesh Roy, Chairman, InsPIRE

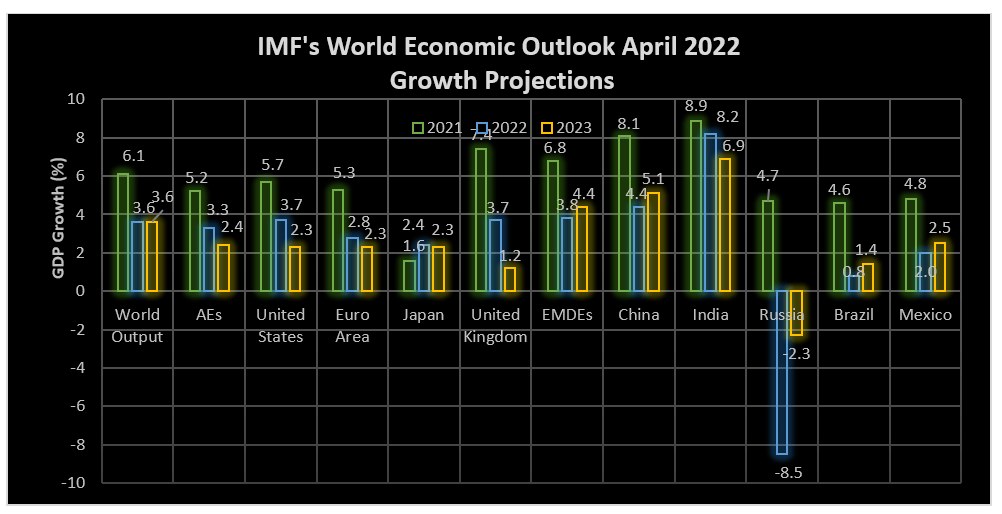

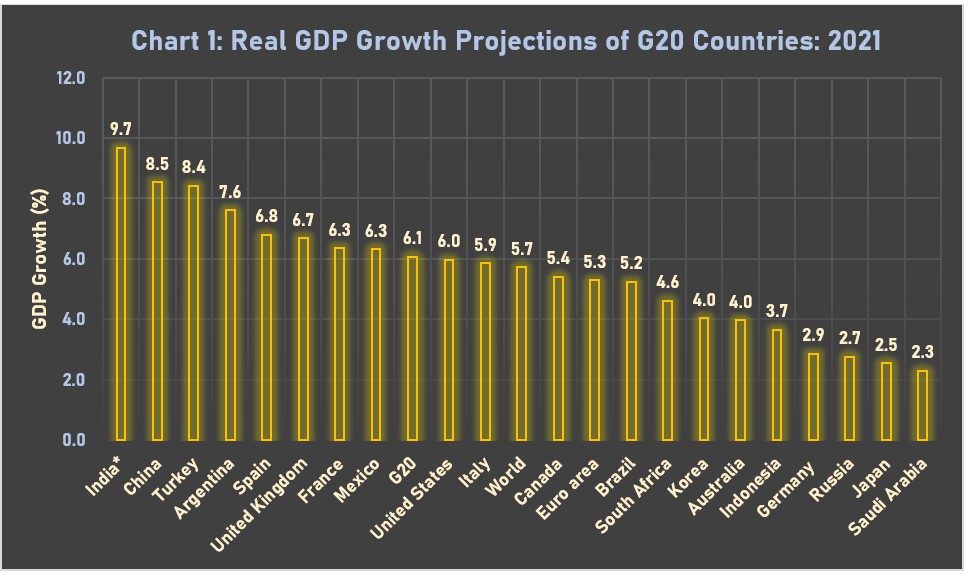

The International Monetary Fund (IMF) in its April 2022 edition of the World Economic Outlook (WEO) has projected the global economy to slow down sharply from 6.1 percent in 2021 to 3.6 percent in 2022 and 2023. The projections are 0.8 and 0.2 percentage points lower for 2022 and 2023, respectively, made in the January 2022 WEO Update.

Beyond 2023, global growth is forecast to decline to about 3.3 percent over the medium term. The sharp cut in growth projections is the result of the humanitarian and economic impact of Russia-Ukraine war, and the sanctions against Russia imposed by the United States (US) and its allies. Crucially, the projections by IMF assume that the conflict remains confined to Ukraine, further sanctions on Russia exempt the energy sector and the pandemic’s health and economic impacts weaken during 2022. Further, employment and output will remain below pre-pandemic trends through 2026, with few exceptions.

The IMF warns that unusually high uncertainty surrounds the growth forecast, and downside risks to the global outlook dominate—including from a possible worsening of the war, escalation of sanctions on Russia, a sharper-than-anticipated deceleration in China from 8.1 per cent in 2021 to 4.4 per cent in 2022. Moreover, the war in Ukraine has increased the probability of wider social tensions because of higher food and energy prices, which would further weigh on the outlook.

The advanced economies (AEs) are expected to slow-down sharply from 5.2 per cent in 2021 to 3.3 per cent in 2022 and 2.4 per cent in 2023, as shown in the chart below. The US is expected to witness a sharp fall in growth from 5.7 per cent in 2021 to 3.7 in 2022 and 2.3 per cent in 2023. The Euro area, too, is estimated to slowdown from 5.3 per cent in 2021 to 2.8 per cent and 2.3 per cent in 2022 and 2023, respectively.

The growth of emerging market and developing economies (EMDEs) is expected to fall sharply from 6.8 per cent in 2021 to 3.8 per cent in 2022, but would rise to 4.4 per cent in 2023. The projected growth rates for AEs as well as EMDEs have been downgraded from the projections made by the IMF in October 2021 and January 2022, in view of the ongoing Russia-Ukraine war, disruption in global supply chains and unprecedented world-wide inflationary situation.

The IMF downgraded India’s growth forecast for FY23 from 9 per cent estimated in January 2022 to 8.2 per cent, citing the impact of high oil prices on consumer demand and private investments. The forecast for India by the IMF is among the most optimistic so far. While the RBI lowered India’s growth projection for FY23 from 7.8 per cent estimated earlier to 7.2 per cent in the latest Monetary Policy Committee (MPC) meeting (06-08 April 2022), the World Bank reduced India’s growth forecast from 8.7 per cent estimated in January 2022 to 8 per cent, recently. However, India is projected to remain the world’s fastest-growing major economy by the IMF, the World Bank and the OECD. But we live in an uncertain world, and the actual growth could end up below the projections.

The IMF has identified the following five principal forces that would shape the near-term global outlook:

The war in Ukraine

The economic damage will lead to a significant slowdown in global growth in 2022 – a severe double-digit drop in GDP for Ukraine and an 8.5 per cent contraction in Russia, along with spillovers across the world through commodity markets, trade, and financial channels.

Monetary tightening and financial market volatility

Significant rise in inflation in major economies has led to tightening of monetary policy by central banks. This has contributed to a rapid increase in nominal interest rates across advanced economy sovereign borrowers. In the months ahead, policy rates are generally expected to rise further and central banks would begin to unwind balance sheets in AEs and also in several EMDEs. Capital outflows from EMDEs have led to sharp fluctuations in the financial markets in these economies. Further, the financial markets across the globe have been experiencing sharp fluctuations due to the imminent rise in US Fed rates.

Fiscal withdrawal

Policy space in many countries has been eroded by necessary higher COVID-related spending and lower tax revenue in 2020–21. Faced with rising borrowing costs, governments are increasingly challenged by the imperative to rebuild buffers.

China’s slowdown

Deceleration in China’s economic growth has wider ramifications for Asia and for commodity exporters.

Pandemic and vaccine access

Restrictions have begun to ease as the peak of the Omicron wave passes and global weekly COVID deaths decline. The risk of infection leading to severe illness or death appears lower for the dominant Omicron strain than for others—especially for the vaccinated and boosted. The health and economic impacts of the virus are expected to start to fade in the second quarter of 2022.