Bijetri Roy, Managing Director & Chief Strategy Officer, InsPIRE

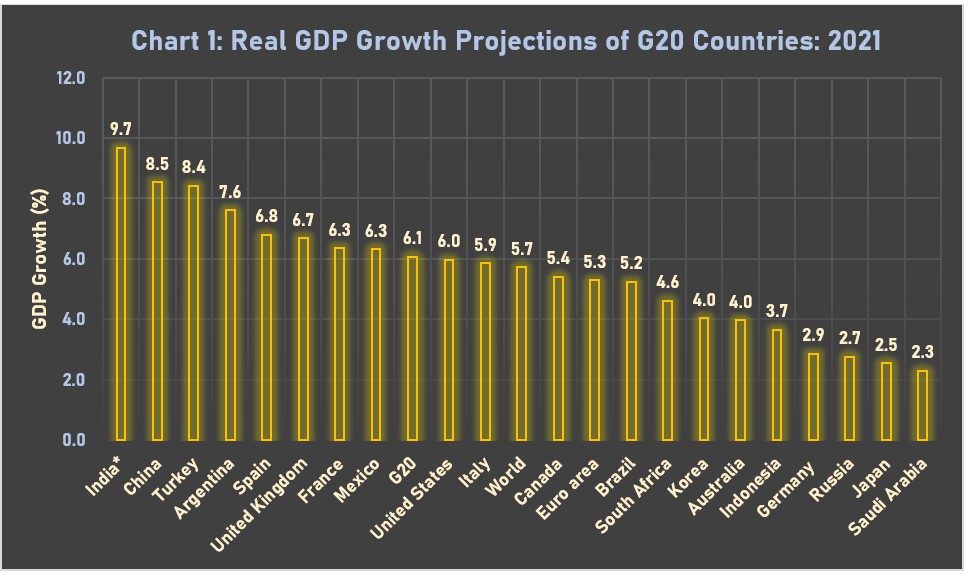

The OECD, in its interim report for September 2021, has projected a strong, but uneven global growth in the years 2021 and 2022 (Charts 1 and 2). Government and central bank support and progress in vaccination would lead to growth above the pre-pandemic level. With countries emerging from the crisis facing different challenges, the growth would remain uneven.

Wide differences in vaccination rates between countries and emergence of new variants of the virus have restricted the opening up of economies and affected the supply chains. Output and employment gaps continue in many countries, especially in emerging-market and developing economies (EMDEs), where vaccination rates are low.

Estimates by OECD indicate that global GDP would grow at 5.7% in 2021 (Chart 1), followed by 4.5% in 2022 (Chart 2). The GDP has now surpassed its pre-pandemic level, but output in mid-2021 was still 3.5% below the projection made before the pandemic. This indicates a real income shortfall of over $ 4.5 trillion (in 2015 PPPs). It is, therefore, imperative to close this gap to minimise long-term damage to the global economy from the pandemic through job and income losses.

G20 countries are expected to grow at 6.1% in 2021 (Chart 1) and 4.1% in 2022 (Chart 2), mainly driven by high growth in India (9.7%), China (8.5%), Turkey (8.4%), and Argentina (7.6%) in 2021. The year 2022 could witness a slower, although a stable growth due to pick up in investments and consumption, without the benefit of base effect. Growth in GDP in 2022 is expected to be influenced by India (7.9%), Spain (6.6%) and China (5.8%).

As indicated by high-frequency activity indicators, such as the Google location-based measures of retail and recreation mobility, global activity continued to strengthen in recent months, helped by improvements in Europe and a strong rebound in India and Latin American countries.

India is set to regain its position as the fastest growing economy in the world. According to OECD, India is expected to grow at a real GDP of 9.7% in 2021-22 (Chart 1), albeit from a low base. However, the Indian economy is expected to get on track to a long-term high growth trajectory, with a brisk growth of 7.9% in 2022-23 (Chart 2).

The Q1 (April-June 2021) GDP figures, the latest core sector growth data and recent positive high frequency activity data, indicate that the economy is gaining traction. Standard & Poor’s has also highlighted in a recent Asia Pacific report that India’s growth in GDP would make a strong rebound in the July-September 2021 quarter, but warned against the impact of faster than expected tapering by the US Federal Reserve, causing capital flow risks as monetary policy by Reserve Bank of India (RBI) remains accommodative with real rate of interest in negative territory.

However, tapering by US Federal Reserve is expected to be gradual and EMDEs like India may not face an adverse situation similar to the taper tantrum of 2013. Moreover, India’s economic fundamentals are getting stronger, and the country could grow at a faster and more sustainable rate.

The Chinese economy is showing signs of a slowdown in economic growth. Troubles are brewing in the real estate and energy sectors in China. The country is facing an energy crunch due to shortages of coal for power generation, forcing it to increase purchase of natural gas. China’s power demand increased by 15% during the current year, but its domestic supply of coal – the largest source of power generation in the country – grew by just 5%. The Evergrande crisis has shown the fragility of the real estate sector in the country. If that is not all, the Chinese government’s recent crackdown on large corporations could impact investment and growth adversely.

Source: OECD Economic Outlook, Interim Report September 2021

Source: OECD Economic Outlook, Interim Report September 2021.

The global economy continues to be in a state of flux. There is ample evidence to suggest that the supply shock reverberating around the world, combined with outbreaks of the Delta variant of corona virus, is tempering the recovery in growth. Results of business surveys from the US, UK and Eurozone suggest that economic activities have slowed down as delivery times grew longer and backlogs built up.

Policy Measures to Support Global Growth Prescribed by OECD

Governments need to ensure deployment of all resources necessary to accelerate vaccinations throughout the world to save lives, preserve incomes and control the virus. Also, there is need for stronger international efforts to support vaccinations in low-income countries.

Continuance of macroeconomic policy support, with the mix of policies contingent on economic developments in each country.

Maintenance of accommodative monetary policy, with a clear guidance about the horizon and extent to which any inflation overshooting will be tolerated. Also, there needs to be a clear roadmap towards normalisation of monetary policy.

Fiscal policies should remain flexible and contingent on the state of the economy.

Credible fiscal frameworks that provide clear guidance about the medium-term path towards debt sustainability, and likely policy changes along that path, to help maintain confidence and enhance the transparency of budgetary choices.

There is a need for stronger public investment and enhanced structural reforms for boosting resilience, and improving the prospects for sustainable and equitable growth.