Dr Debesh Roy, Chairman, InsPIRE

The prospects for India’s real GDP growth for 2021-22 received a setback with the latest official projection (second advance estimate of NSO, MoSPI, GoI on 28 February 2022) dropping to 8.9 per cent (Figure 1) from 9.2 per cent (first advance estimate on 07 January 2022). However, the quantum of real GDP, has been estimated to increase from INR147.54 trillion (USD 1.95 trillion) (FAE) to INR 147.72 trillion (USD 1.95 trillion) (SAE). The growth of nominal GDP was revised upward from 17.6 per cent to 19.4 per cent, with the quantum of nominal GDP witnessing an uptick from INR 232.15 trillion (USD 3.06 trillion) to INR 236.44 trillion (USD 3.12 trillion) (SAE). The real GDP growth estimate for the previous fiscal year showed an improvement to -6.6 per cent (first revised estimate) from -7.3 per cent (provisional estimate).

Source: Based on data accessed from MoSPI, GoI

India’s third quarter (Q3) real GDP fell sharply to 5.4 per cent from 8.5 per cent (Q2) and 20.3 per cent (Q1) (Figure 2).

Projections of India’s real GDP growth for FY 22 and FY23 are presented in the following table. The lowest estimate for FY 22 is 8.7 per cent by the World Bank and the highest is 9.4 per cent by OECD. The highest projection for FY 23 at 8-8.5 percent has been estimated in the Economic Survey 2021-22 (MoF, GoI) and the lowest is by the World Bank at 6.8 per cent.

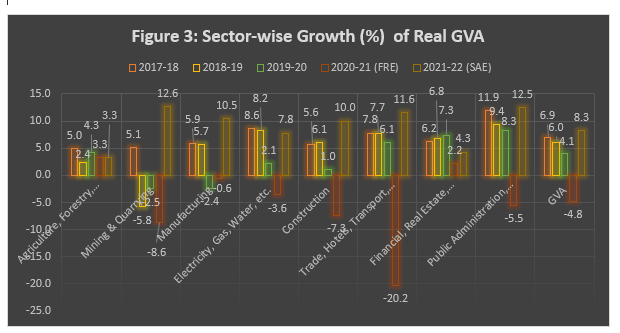

India’s real GVA is estimated to grow at 8.3 per cent (SAE) in FY22, downgraded from 8.6 per cent (FAE) (Figure 3). The sectors which witnessed high growth are mining and quarrying (12.6 per cent from a low base of -8.6 per cent in FY21), public administration (12.5 per cent from -5.5 per cent), manufacturing (10.5 per cent from -0.6 per cent), and trade, hotels, transport, etc. (11.6 per cent from -20.2 per cent). While the agriculture sector is estimated to grow at a constant rate of 3.3 per cent as in the previous year, financial, real estate and professional sector is estimated to grow at 4.3 per cent (from 2.2 per cent in FY 21) (Figure 3).

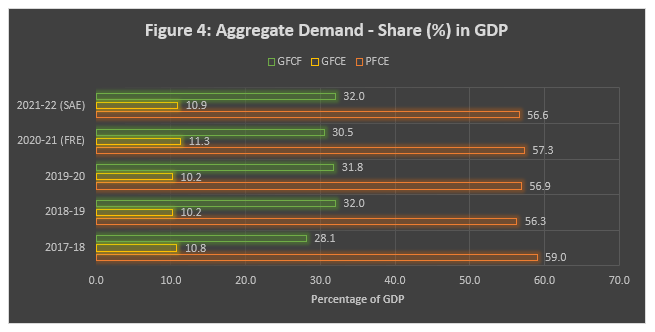

India’s growth has traditionally been consumption-led, and the share of private final consumption expenditure (PFCE) in GDP is estimated to decline to 56.6 per cent in FY22 (SAE) from 57.3 per cent in FY21 (Figure 4). The pandemic-induced loss of income and livelihood opportunities in the contact intensive service sector, the informal sector and rural areas, are expected to dampen India’s growth prospects for FY22. However, GoI’s thrust on investment in infrastructure, could lead to high and sustainable growth in income, employment and economic growth. While the estimated increase in the share of gross fixed capital formation (GFCF) from 30.5 per cent in FY21 to 32 per cent in FY22, is a stimulant for growth, the share of government final consumption expenditure (GFCE) which is estimated to decline from 11.3 per cent to 10.9 per cent, could drag down growth. However, the FY 23 Union Budget’s focus on investment in infrastructure with a significantly higher allocation over that of the previous Budget, would crowd in private investment and enable India to grow at around 8 per cent, while continuing to be the fastest growing large economy in the world.

The economic impact of the third wave of the pandemic has not been as severe as that of the previous waves. The impact of global headwinds like the Russia-Ukraine conflict and the consequent sharp rise in the prices of crude oil and commodity prices, have not been factored in these estimates, and therefore, the final growth print could be 1-2 per cent lower. About 85 per cent of India’s demand for crude oil is met from imports and with the recent sharp rise in Brent crude price to USD 130/ barrel, there would be a sharp rise in the country’s import bill, worsening the country’s current account deficit. This would also lead to a sharper rise in retail inflation, which has already crossed RBI’s upper tolerance limit of 6 per cent. The RBI has continued with its accommodative stance with a view to revving up economic growth. However, with worsening inflationary expectations, the RBI could switch to a neutral stance, and could consider raising the repo rate by 25 bps in the next MPC meeting in April 2022 or in the June 2022 meeting. The developed economies are suffering from the worst phase of inflation in the last 3-4 decades, and the Central Banks in these countries have started tightening liquidity. The US Federal Reserve is expected to raise the Fed rate from the present near zero rate by 25 basis points, in March 2022, and at least two-three more rate hikes during the year.

The Russia-Ukraine conflict has also eroded financial markets globally, including India. Russian strikes at Europe’s largest nuclear plant in Ukraine wiped INR 5 trillion (USD 66 billion) off investor wealth in India on 04 March 2022, with the geopolitical tension eroding about INR 15 trillion ($197 billion) in fortune from 15 February 2022, when Russia announced a partial withdrawal of its troops from Ukrainian border only to launch a full-scale invasion later on.

Geopolitics could erode India’s growth prospects, depending on how long the Russia-Ukraine conflict and the consequent sanctions against Russia would continue. However, if the conflict ends within the next few months, and India gives a big push to investment in infrastructure, the country’s growth prospects could improve, and a 7.8 – 8 per cent growth in FY23 could be achievable.