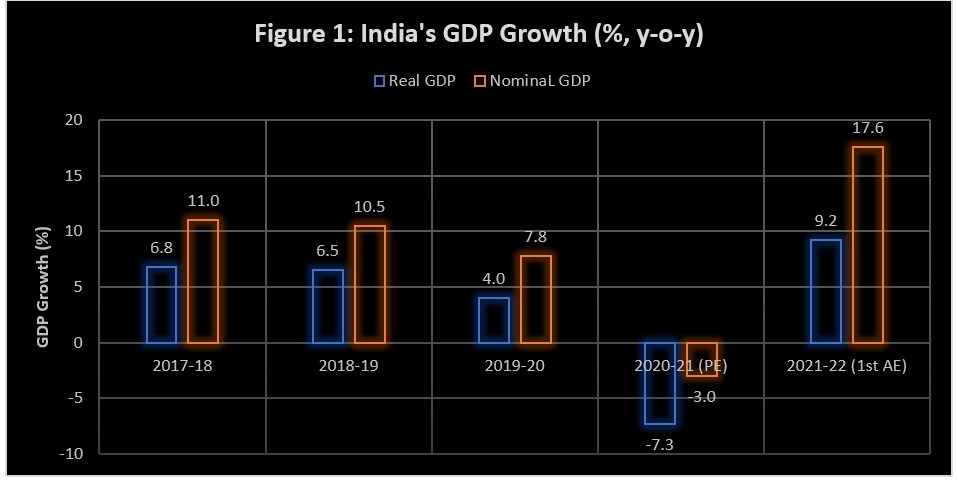

The prospects for India’s real GDP growth for 2021-22 received a setback with the latest official projection (second advance estimate of NSO, MoSPI, GoI on 28 February 2022) dropping to 8.9 per cent (Figure 1) from 9.2 per cent (first advance estimate on 07 January 2022). However, the quantum of real GDP, has been estimated to increase from INR147.54 trillion (USD 1.95 trillion) (FAE) to INR 147.72 trillion (USD 1.95 trillion) (SAE). The growth of nominal GDP was revised upward from 17.6 per cent to 19.4 per cent, with the quantum of nominal GDP witnessing an uptick from INR 232.15 trillion (USD 3.06 trillion) to INR 236.44 trillion (USD 3.12 trillion) (SAE). The real GDP growth estimate for the previous fiscal year showed an improvement to -6.6 per cent (first revised estimate) from -7.3 per cent (provisional estimate).

Note: FRE: First Revised Estimate; SAE: Second Advance Estimate Source: Based on data accessed from MoSPI, GoI

India’s third quarter (Q3) real GDP fell sharply to 5.4 per cent from 8.5 per cent (Q2) and 20.3 per cent (Q1) (Figure 2).

Source: Based on data accessed from MoSPI, GoI

Projections of India’s real GDP growth for FY 22 and FY23 are presented in the following table. The lowest estimate for FY 22 is 8.7 per cent by the World Bank and the highest is 9.4 per cent by OECD. The highest projection for FY 23 at 8-8.5 percent has been estimated in the Economic Survey 2021-22 (MoF, GoI) and the lowest is by the World Bank at 6.8 per cent.

Source: (1) MoSPI, GoI, and Economic Survey 2021-22, MoF, GoI; (2) Monetary Policy Statement February 10, 2022, RBI; (3) Ecowrap, February 28, 2022, SBI; (4) World Economic Outlook, January 2022, IMF; (5) Global Economic Prospects, January 2022, World Bank; (6) India Economic Outlook, OECD, December 2021

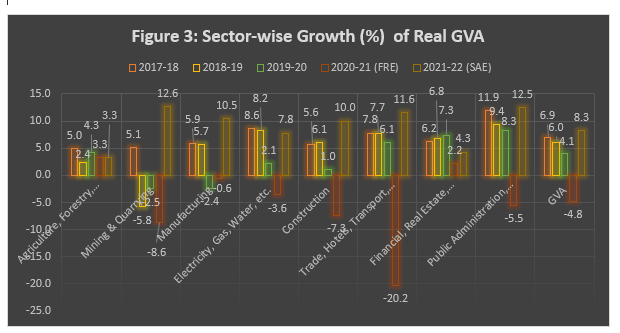

India’s real GVA is estimated to grow at 8.3 per cent (SAE) in FY22, downgraded from 8.6 per cent (FAE) (Figure 3). The sectors which witnessed high growth are mining and quarrying (12.6 per cent from a low base of -8.6 per cent in FY21), public administration (12.5 per cent from -5.5 per cent), manufacturing (10.5 per cent from -0.6 per cent), and trade, hotels, transport, etc. (11.6 per cent from -20.2 per cent). While the agriculture sector is estimated to grow at a constant rate of 3.3 per cent as in the previous year, financial, real estate and professional sector is estimated to grow at 4.3 per cent (from 2.2 per cent in FY 21) (Figure 3).

Source: Based on data accessed from MoSPI, GoI

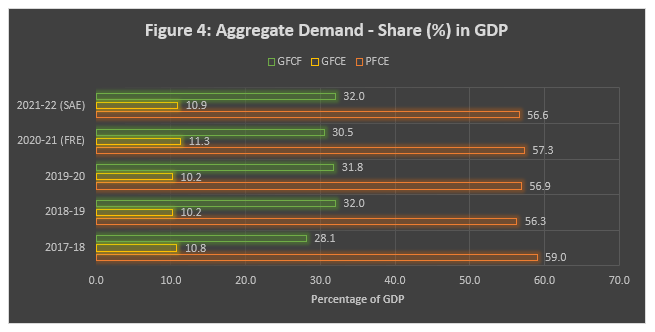

India’s growth has traditionally been consumption-led, and the share of private final consumption expenditure (PFCE) in GDP is estimated to decline to 56.6 per cent in FY22 (SAE) from 57.3 per cent in FY21 (Figure 4). The pandemic-induced loss of income and livelihood opportunities in the contact intensive service sector, the informal sector and rural areas, are expected to dampen India’s growth prospects for FY22. However, GoI’s thrust on investment in infrastructure, could lead to high and sustainable growth in income, employment and economic growth. While the estimated increase in the share of gross fixed capital formation (GFCF) from 30.5 per cent in FY21 to 32 per cent in FY22, is a stimulant for growth, the share of government final consumption expenditure (GFCE) which is estimated to decline from 11.3 per cent to 10.9 per cent, could drag down growth. However, the FY 23 Union Budget’s focus on investment in infrastructure with a significantly higher allocation over that of the previous Budget, would crowd in private investment and enable India to grow at around 8 per cent, while continuing to be the fastest growing large economy in the world.

Source: Based on data accessed from MoSPI, GoI

The economic impact of the third wave of the pandemic has not been as severe as that of the previous waves. The impact of global headwinds like the Russia-Ukraine conflict and the consequent sharp rise in the prices of crude oil and commodity prices, have not been factored in these estimates, and therefore, the final growth print could be 1-2 per cent lower. About 85 per cent of India’s demand for crude oil is met from imports and with the recent sharp rise in Brent crude price to USD 130/ barrel, there would be a sharp rise in the country’s import bill, worsening the country’s current account deficit. This would also lead to a sharper rise in retail inflation, which has already crossed RBI’s upper tolerance limit of 6 per cent. The RBI has continued with its accommodative stance with a view to revving up economic growth. However, with worsening inflationary expectations, the RBI could switch to a neutral stance, and could consider raising the repo rate by 25 bps in the next MPC meeting in April 2022 or in the June 2022 meeting. The developed economies are suffering from the worst phase of inflation in the last 3-4 decades, and the Central Banks in these countries have started tightening liquidity. The US Federal Reserve is expected to raise the Fed rate from the present near zero rate by 25 basis points, in March 2022, and at least two-three more rate hikes during the year.

The Russia-Ukraine conflict has also eroded financial markets globally, including India. Russian strikes at Europe’s largest nuclear plant in Ukraine wiped INR 5 trillion (USD 66 billion) off investor wealth in India on 04 March 2022, with the geopolitical tension eroding about INR 15 trillion ($197 billion) in fortune from 15 February 2022, when Russia announced a partial withdrawal of its troops from Ukrainian border only to launch a full-scale invasion later on.

Geopolitics could erode India’s growth prospects, depending on how long the Russia-Ukraine conflict and the consequent sanctions against Russia would continue. However, if the conflict ends within the next few months, and India gives a big push to investment in infrastructure, the country’s growth prospects could improve, and a 7.8 – 8 per cent growth in FY23 could be achievable.

The Union Budget 2022-23 is refreshingly growth oriented, futuristic and at the same time it aims to promote all-inclusive welfare. India’s economic growth which was already on a decelerating mode from 7.2% in 2017-18 to 6.1% in 2018-19 and further down to 4% in 2019-20, due to structural issues, and loss of momentum in economic reforms, fell sharply to -7.3% in 2020-21, as a result of the pandemic (Figure 1). However, the year 2021-22 is poised to reverse the trend to touch 9.2%, and India is set to regain its status as the fastest growing large economy.

Source: MoSPI, GoI

There are, however, looming headwinds like retail inflation breaching RBI’s upper tolerance limit of 6% (6.01% in January 2022) on account of rising food prices, international crude oil prices, with the Brent crude oil price hovering around $96 per barrel, and inching towards $100 per barrel, due to strong demand and supply disruptions as a result of the Ukraine crisis. The imminent speeding up of hikes in the Fed rate, and the consequent flight of capital from emerging market economies like India, could depreciate the Indian rupee further and could worsen the inflationary situation. Further, loss of lives and livelihoods, and consequently slow growth in consumption demand, along with weak growth in contact intensive sectors due to the pandemic, could prove to be a drag on the economy, if they persist for some more time.

Investment in Infrastructure for Turbo-charging the Indian Economy

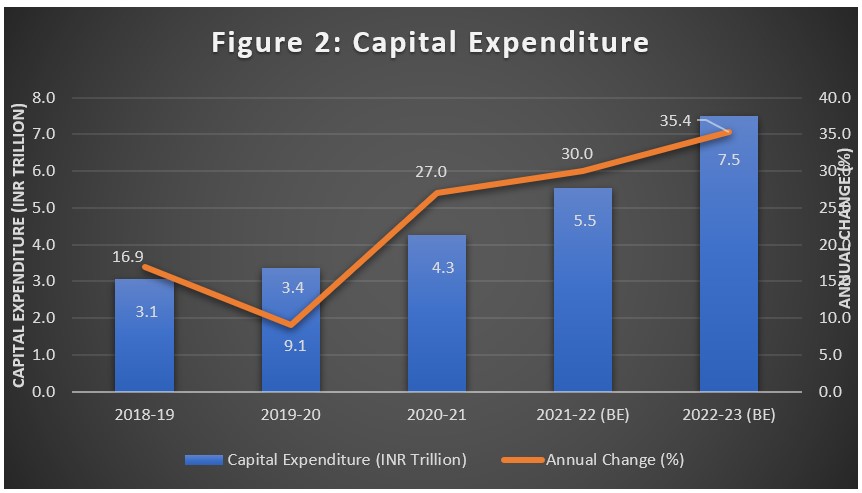

The Budget has done well to focus on the achievement of high, sustainable and inclusive growth. It has proposed a significantly higher allocation of 35.4% to capital expenditure to INR 7.5 trillion compared to INR 5.54 trillion in the previous year’s Budget, which is a continuance of strong growth in capital expenditure during 2020-21(actual) and 2021-22 (budget estimate) (Figure 2).

Source: Expenditure Profile (various issues), Ministry of Finance, Budget Division, GoI

The basic philosophy behind the Budget is to spend more in the core sector and accelerate growth. A massive release of funds for infrastructure projects will stimulate a large number of core sector suppliers such as steel and cement, which will create more jobs and increase economic demand and boosting growth in the economy. Investments in infrastructure is said to have a multiplier effect of four times of the money spent. As asserted by the Union Finance Minister Ms. Nirmala Sitharaman: “ Even if private investment is taking a while to come into this whole scene, the government will have to spend and pull the economy forward and gradually as we do this, we expect the private investment to come out in full force.”

The present Budget has carried forward the focus on investment in infrastructure for boosting economic growth, along with a focus on health and wellbeing of the people in the Union Budget 2021-22. The pillars on which the previous Budget rested were: health and wellbeing; physical and financial capital and infrastructure; inclusive development for an aspirational India; reinvigorating human capital; innovation and R&D; and minimum government and maximum governance. The Budget 2022-23 carries forward the pillars of the previous Budget, but adopts certain goals for the next quarter century – the Amrit Kaal – setting a blueprint for the vision of India@100, viz. complementing the macro-economic level growth focus with a micro-economic level all-inclusive welfare focus; promoting digital economy & fintech, technology enabled development, energy transition, and climate action; and relying on virtuous cycle starting from private investment with public capital investment helping to crowd-in private investment.

The four priorities for achieving the vision for India@100 articulated in the Budget are: PM Gati Shakti; Inclusive Development; Productivity Enhancement & Investment, Sunrise Opportunities, Energy Transition, and Climate Action; and Financing of Investments. PM Gati Shakti is driven by seven engines, viz. roads, railways, airports, ports, mass Transport, waterways, and logistics infrastructure. The aim is to bring about seamless multimodal movement of goods and people, which would lead to overall improvement of efficiency in the economy and ease of living. The PM Gati Shakti National Master Plan aims to bring about world class modern infrastructure and logistics synergy. This would lead to improvement in productivity and acceleration in economic growth and development on a sustainable basis.

Ecologically sustainable connectivity in hilly areas, through National Ropeways Development Programme, proposed to be taken up on PPP mode, would not only provide a convenient mode of transport, but would also promote tourism. The programme will also cover congested urban areas.

The Prime Minister’s Development Initiative for North- East (PM-DevINE), a new scheme for the development of the North Eastern States, with an initial allocation of INR15 billion, will fund infrastructure, in the spirit of PM Gati Shakti, and social development projects based on felt needs of the region The scheme will enable livelihood activities for youth and women,

The strengthening of health infrastructure, speedy implementation of the vaccination programme, and the nation-wide resilient response to the current wave of the pandemic, have been at the top of GoI’s agenda, for dealing with the present pandemic scenario, and making the country future ready to effectively address and manage pandemic situations.

Inclusive Growth and Welfare

Apart from the massive investment proposed for infrastructure, the Budget also prioritizes inclusive welfare and growth, while giving a short shrift to politically convenient sops and subsidies. Some of the prominent announcements for attaining inclusive growth are as follows:

Modernizing the agriculture sector

Delivery of digital and hi-tech services to farmers with involvement of public sector research and extension institutions along with private agri-tech players and stakeholders of agri-value chain, a scheme in PPP mode; promoting ‘Kisan Drones’ for crop assessment, digitization of land records, spraying of insecticides, and nutrients; promoting zero-budget and organic farming, modern-day agriculture, value addition and management; raising fund with blended capital, under the co-investment model, facilitated through NABARD, to finance startups for agriculture & rural enterprise, which will support FPOs, machinery for farmers on rental basis at farm level, and technology including IT-based support; implementing the Ken-Betwa Link Project, at an estimated cost of INR 446.05 billion, aimed at providing irrigation benefits to 0.91 million hectare of farmers’ lands, drinking water supply for 6.2 million people, 103 MW of Hydro, and 27 MW of solar power; support to concerned states for implementing the linking of five rivers, viz. Damanganga-Pinjal, Par-Tapi-Narmada, Godavari-Krishna, Krishna-Pennar and Pennar-Cauvery; a comprehensive package for promoting food processing with participation of state governments, which would facilitate farmers to adopt suitable varieties of fruits and vegetables, and to use appropriate production and harvesting techniques.

Revamping the MSME Sector

Interlinking Udyam, e-Shram, NCS and ASEEM portals, to provide services related to credit facilitation, skilling, and recruitment with an aim to further formalise the economy and enhance entrepreneurial opportunities for all; extending Emergency Credit Line Guarantee Scheme (ECLGS) up to March 2023 and expanding its guarantee cover by INR 500 billion to total cover of INR 5 trillion, with the additional amount being earmarked exclusively for the hospitality and related enterprises; revamping the Credit Guarantee Trust for Micro and Small Enterprises (CGTMSE) scheme to facilitate additional credit of INR 2 trillion for Micro and Small Enterprises and expand employment opportunities; and rolling out the Raising and Accelerating MSME Performance (RAMP) programme with outlay of INR 60 billion over 5 years to help the MSME sector become more resilient, competitive and efficient.

Creating a Strong Digital Ecosystem

Aligning the National Skill Qualification Framework (NSQF) with dynamic industry needs; launching Digital Ecosystem for Skilling and Livelihood – the DESH-Stack e-portal; promoting startups to facilitate ‘Drone Shakti’ through varied applications and for Drone-As-A-Service (DrAAS); Establishing Digital University to provide access to students across the country for world-class quality universal education with personalised learning experience at their doorsteps; rolling out an open platform, for the National Digital Health Ecosystem; and launching a ‘National Tele Mental Health Programme’ to improve the access to quality mental health counselling and care services.

Women Empowerment and Child Development

Mission Shakti, Mission Vatsalya, Saksham Anganwadi and Poshan 2.0 were launched recently to provide integrated benefits to women and children. The new generation The Budget has proposed to upgrade 0.2 million anganwadis to Saksham Anganwadis, with improved infrastructure.

Housing and Drinking Water for All

Universal coverage of low-cost housing and access of every household to tapped drinking water, aim at ease of living for all.Therefore, under the PM Awas Yojana, 8 million houses are expected to be completed during 2022-23. Currently, 87 million households have access to drinking water under Har Ghar, Nal Se Jal. The scheme aims to cover 38 million households in 2022-23.

Addressing Rural-Urban Divide

Aspirational Districts Programme

Under the Aspirational Districts Programme improvement in the quality of life of citizens in the most backward districts of the country has been observed, 95% of those 112 districts having made significant progress in key sectors such as health, nutrition, financial inclusion and basic infrastructure, surpassing the state average values. However, some blocks in those districts, continue to lag. Therefore, in 2022-23, the programme will focus on such blocks in those districts, under the Aspirational Blocks Programme.

Vibrant Villages Programme

A new Vibrant Villages Programme will be implemented in villages on the northern border, with sparse population, limited connectivity and infrastructure. The activities under the programme will include construction of village infrastructure, housing, tourist centres, road connectivity, provisioning of decentralized renewable energy, direct to home access for Doordarshan and educational channels, and support for livelihood generation. Existing schemes will be converged with this programme.

Digital Financial Inclusion

Post Offices under core banking system

100% of 1.5 lakh post offices will come on the core banking system enabling financial inclusion and access to accounts through net banking, mobile banking, ATMs, and also provide online transfer of funds between post office accounts and bank accounts.

Digital Banking Units

75 Digital Banking Units (DBUs) are proposed to be set up in 75 districts of the country by Scheduled Commercial Banks.

Financial support for digital payment

Financial support for digital payment ecosystem announced in the previous Budget will continue in 2022-23.

Productivity Enhancement

Major sectors of the Indian economy need to become globally competitive, if India is to grow rapidly and sustainably over the next quarter of a century to transform itself into a global economic powerhouse. Some of the major announcements in this regard are as under:

Ease of Doing Business 2.0 & Ease of Living

The next phase of EODB and Ease of Living would aim to improve productive efficiency of capital and human resources, with the government following the idea of ‘trust-based governance’. Active involvement of the states, digitization of manual processes and interventions, integration of the central and state-level systems through IT bridges, a single point access for all citizen-centric services, and a standardization and removal of overlapping compliances, are expected.

Energy Transition, Climate Action and Circular Economy

The Hon’ble Prime Minister of India, at the COP26 summit in Glasgow had said, “what is needed today is mindful and deliberate utilization, instead of mindless and destructive consumption.” The low carbon development strategy indicates the government’s strong commitment towards sustainable development. The Budget has announced the following short-term and long-term actions:

Additional allocation for PLI

An additional allocation of INR195 billion for PLI for manufacture of high efficiency modules, in order to facilitate domestic manufacturing for achieving the ambitious goal of 280 GW of installed solar capacity by 2030.

Transition to circular economy

The transition to circular economy is expected to help in productivity enhancement as well as creating large opportunities for new businesses and jobs. While the action plans for ten sectors such as electronic waste, end-of-life vehicles, used oil waste, and toxic & hazardous industrial waste are ready, the Budget identifies policy focus on addressing important cross cutting issues of infrastructure, reverse logistics, technology upgradation and integration with informal sector.

Transition to carbon neutral economy

While five to seven per cent biomass pellets will be co-fired in thermal power plants resulting in CO2 savings of 38 MMT annually, it will also provide extra income to farmers and create job opportunities, while helping avoid stubble burning in agriculture fields.

Urban Development

India @100 will have nearly half its population living in urban areas. The government plans to nurture the megacities and their hinterlands to become current centres of economic growth and also to facilitate tier 2 and 3 cities to take on the mantle in the future to realise the country’s economic potential, including livelihood opportunities for the demographic dividend. States would be involved as partners in the process of urban planning and development, with financial support from the Central Government. The government also plans to promote a shift to use of public transport in urban areas, which will be complemented by clean tech and governance solutions, special mobility zones with zero fossil-fuel policy, and EV vehicles.

Telecom Sector

The Budget highlights the importance of telecommunication in general, and 5G technology in particular, as an enabler of growth and creation of employment opportunities. Spectrum auctions will, therefore, be conducted in 2022 to facilitate rollout of 5G mobile services within 2022-23 by private telecom providers. Further, a scheme for design-led manufacturing will be launched to build a strong ecosystem for 5G as part of the PLI Scheme.

Export Promotion

India needs to develop into an export-led economy if it is to grow into a $40 trillion economy by India@100. The Budget has announced that the Special Economic Zones Act will be replaced with a new legislation that will enable the states to become partners in ‘Development of Enterprise and Service Hubs’. This will cover all large existing and new industrial enclaves to optimally utilize available infrastructure and enhance competitiveness of exports.

Development of Sunrise Sectors

The Budget underscores the immense potential of Artificial Intelligence, Geospatial Systems and Drones, Semiconductor and its eco-system, Space Economy, Genomics and Pharmaceuticals, Green Energy, and Clean Mobility Systems, in achieving sustainable development at scale, modernizing the country, and also in creating employment opportunities for the youth, while making Indian industry more efficient and competitive.

Mission $40 trillion by India@100

The Union Budget 2022-23 is futuristic and has presented a blueprint to transform India into a leading global economic power by the year 2047. India’s nominal GDP in 2021-22 is estimated at INR 232.1 trillion, which is just over $3.1trillion, well short of $5 trillion by 2024-25.

Can India become a $40 trillion economy by India@100?

While the target may seem humongous, the basic ingredients for achieving the vision have been presented in the Budget, with a focus on investment in infrastructure and other capital investments, raising overall productivity in major sectors of the economy, export promotion, development of sunrise sectors, modernizing the agriculture and food processing sectors, comprehensive development of the North Eastern Region and aspirational blocks, and climate action for sustainable and inclusive development.

The Indian economy is poised to grow at 9.2% in FY22 (Figure 1) as per the First Advance Estimate of the country’s Gross Domestic Product (GDP) (at 2011-12 prices) estimated by the National Statistical Office (NSO), Ministry of Statistics and Programme Implementation (MoSPI), Government of India. This is against a pandemic-induced contraction of 7.3% suffered by the economy in FY21. The real GDP is estimated to increase by 1.3% over that of the pre-pandemic year (FY20).

It is pertinent to note is that, notwithstanding a favourable base effect, the economy is set to record a higher GDP compared to the pre-pandemic year FY20, due to favourable policy environment, resulting in a positive investment growth, as reflected in the Gross Fixed Capital Formation (GFCF).

The nominal GDP is set to grow at a robust 17.6% in FY 22, compared to -3.0% in FY 21. The FY22 nominal GDP, estimated at INR 232.15 trillion (USD 3.12 trillion) is expected to be 14.1% higher than that of the pre-pandemic year (FY20) at INR 203.51 trillion (USD 2.74 trillion). The economy which was on a decelerating mode during the three pre-pandemic years, (real GDP growth at 6.8%, 6.5% and 4.0% respectively during FY18, FY19 and FY20 and nominal GDP growth at 11.0%, 10.5% and 7.8%, respectively), is set to achieve a robust growth 9.2% (real GDP) and 17.6% (nominal GDP) in FY22 (Figure 1).

Source: MoSPI, GoI

The real Gross Value Added (GVA) in FY22 is estimated to grow at 8.6% (Table 1). The GVA data reveals that all sectors of the economy except ‘trade, hotels, transport, communication and services related to broadcasting’ (which are still 8% below the pre-pandemic level) reached the pre-pandemic level (on constant prices).

The agriculture sector, which was the only sector unaffected by the pandemic in terms of real GVA growth in FY21, is estimated to grow steadily at 3.9%, compared to 3.6% in the previous year and 4.3% in FY20. The industrial sector is expected to achieve a robust recovery, with manufacturing; mining and quarrying; electricity, gas and water supply; and construction, set to grow at 12.5%, 14.3%, 8.5% and 10.7%, respectively (Table 1). Under the services sector, trade, hotels, transport, communication and services related to broadcasting, which was the hardest hit during the pandemic is estimated to grow at a robust 11.9%. However, financial, real estate, and professional services, etc. is estimated to grow at a less impressive 4.0%. Public administration, defence, etc. is estimated to grow at 8.6% (Table 1).

Source: MoSPI, GoI

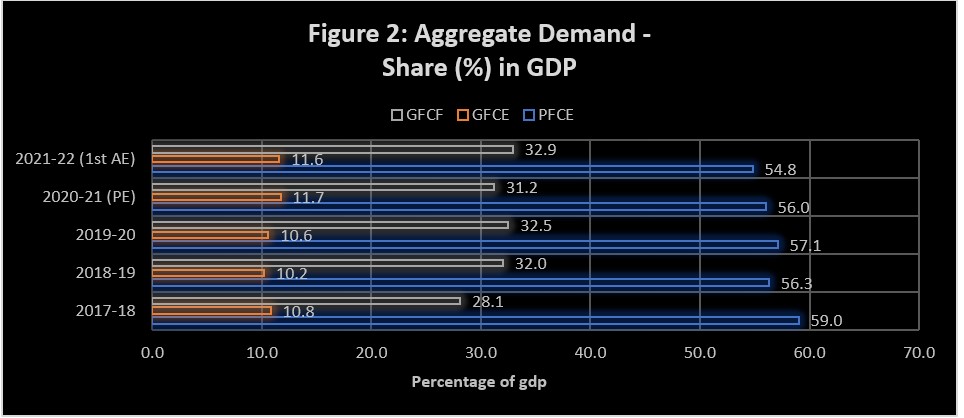

On the expenditure side, Private Final Consumption Expenditure (PFCE) is still 3% below the pre-pandemic level, and its share in GDP is observed to be on a declining trend from 57.1% in FY20, to 56% in FY 21 and further down to 54.8% in FY22 (Figure 2). This is a cause for concern as India’s growth story has essentially been a consumption led one. Loss of lives, livelihoods, jobs and income caused by the pandemic have depressed private consumption.

Another concern is the decline in the share of Government Final Consumption Expenditure (GFCE) in GDP, from 11.7% (FY21) to 11.6% (FY22) (Figure 2). A steady and sustainable growth in GDP can be sustained with a higher share of GFCE, as it crowds in private investment. While fiscal consolidation is of prime importance for attaining high, steady and sustainable growth, it is imperative to recalibrate the same to address the serious impact of the pandemic on the economy.

According to research by SBI (Ecowrap, 07 Jan, 2022), “taking into account the revised GDP figures of today, even if we consider the additional spending announced by the Government in early December 2021 fiscal deficit of the Government still comes at INR 15.88 trillion (USD 0.21 trillion) or 6.8% of the GDP. For FY23, the fiscal consolidation should remain limited to 30-40 bps from the current fiscal”.

A silver lining in the expenditure side is the increase in the share of Gross Fixed Capital Formation (GFCF) in GDP to 32.9% in FY22 (Figure 2), the highest level in the last five years. The primary driver for higher GFCF is the investments made to meet the growing pent-up demand in the economy. The focus of GoI on investment in infrastructure and the Performance Linked Incentive (PLI) Scheme, should lead to accelerated growth in investments, leading to a higher and more sustainable growth in GDP.

Source: MoSPI, GoI

According to the NSO, the First Advance Estimates (FAE) of GDP, introduced in 2016-17 to serve as essential inputs to the Budget exercise, is based on limited data and compiled using the Benchmark-Indicator method i.e., the estimates available for the previous year (2020-21 in this case) are extrapolated using relevant indicators reflecting the performance of sectors.

While there could be some amount of under- or over-estimation of GDP in the FAE, the subsequent estimations, could be within 20-30 basis points, on either side. There could possibly be an upward bias in the revised estimates for FY22. However, it again depends on the impact of the prevailing omicron variant OF Covid-19 on contact-intensive sectors of the economy. Nevertheless, SBI has stuck to its estimate of 9.5% growth in FY22. Earlier estimates by RBI and IMF also point to a 9.5% growth for the Indian economy, while OECD’s estimate is a tad lower at 9.4%, which would still be higher than the growth estimates for China at 8% (IMF) and 8.1% (OECD), making India the fastest growing large economy in the world.

India’s Consumer Price Index (CPI) inflation fell sharply from 5.3% in August 2021 to 4.35% in September 2021, coming closer to RBI’s medium-term inflation target of 4%, and continuing its declining trend for the fourth consecutive month (Figure 1). A sharp decline in food inflation was primarily responsible for the decline in general inflation. While rural inflation dropped to 4.13% in September from 5.28% in the previous month, urban inflation declined from 5.32% to 4.57%. The retail inflation trend for the first half of FY22 reveals a sharp rise from 4.23% in April to 6.3% in May, before tapering to 6.26% and 5.59% in June and July, respectively.

The RBI in its latest Monetary Policy on 8 October 2021 had sharply reduced the outlook for CPI inflation during FY22 from 5.7% projected in the previous MPC meeting (04-06 August 2021) to 5.3%. However, the IMF in its October 2021 issue of World Economic Outlook raised its inflation projection for India from 4.9% estimated in April to 5.6%, citing growing worldwide inflationary risks.

Source: MOSPI, GoI

The main cause for the decline in retail inflation in September is the sharp easing of food inflation (Figure 2). The Consumer Food Price Inflation (CFPI) declined steadily from 5.15% in June 2021 to 3.96% in July and 3.11% in August, before it fell sharply to 0.68% in September. Sharp decline in inflation was observed in respect of vegetables (-11.68% to -22.47%) and eggs (16.33% to 7.06%). Inflation for cereals continued to be negative at -0.61%. However, inflation for edible oils (34.19%) and non-alcoholic beverages (12.99%), remained elevated.

Fuel inflation increased from 12.95% to 13.63%, due to continuous rise in international crude oil prices. Core inflation, which excludes food and fuel prices, however, rose from 5.5% in August to 5.8% in September.

Source: MOSPI, GoI

Further easing of food inflation in the coming months due to good kharif harvest, and favourable base effect, will keep inflation benign. This would give enough leeway to the RBI to continue with the accommodative stance, at least till April 2022 monetary policy review. However, inflation risks remain high due to elevated international commodity prices, including crude oil prices. Further, price pressures could intensify due to the second-round effects of high fuel costs, resulting in higher prices of other goods, after a time lag.

Wholesale Inflation

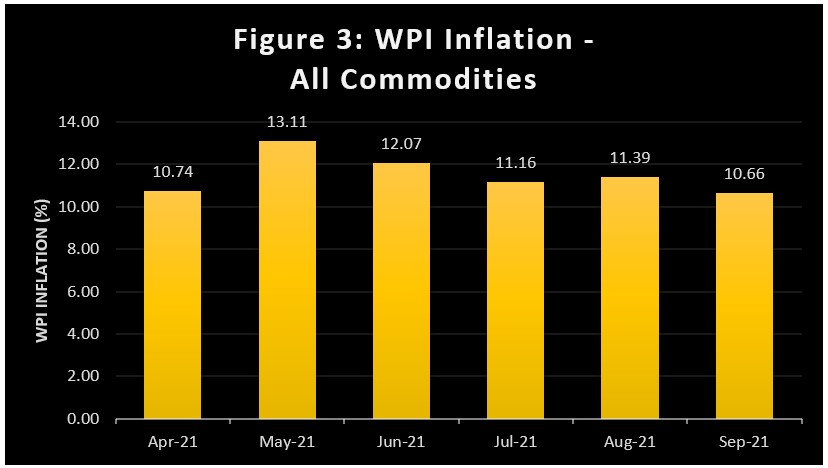

India’s WPI inflation declined to 10.66% in September, the lowest in six months, from 11.39% in August (Figure 3). However, the continued high WPI inflation was on account of high inflation of manufactured products (weight of 64.2%) in May, June, July, August and September at 11.25% 10.96%, 11.2%, 11.39% and 11.41%, respectively.

It is evident that cost push pressures are gradually seeping into prices of manufactured goods, due to increase in manufacturing activities in the post-pandemic situation. The highest inflation was observed in case of crude petroleum and natural gas at 59.5%, 46.97%, 40.28%, 40.03% and 43.92%, respectively, during the last five months, due to steady increase in the international price of crude oil.

Fuel and power inflation at 36.74%, 29.32%, 26.02%, 26.09% and 24.81 respectively in May, June, July, August and September. The decline in WPI inflation was due to reduction in food inflation from -1.29% in August to -4.69% in September, 2021.

Price volatility in the international markets for crude oil and rising prices of edible oils and metal products would lead to further rise in WPI inflation, considering the fact that India is a price taker for most of these commodities.

Source: Office of the Economic Adviser, Ministry of Commerce and Industry, GoI

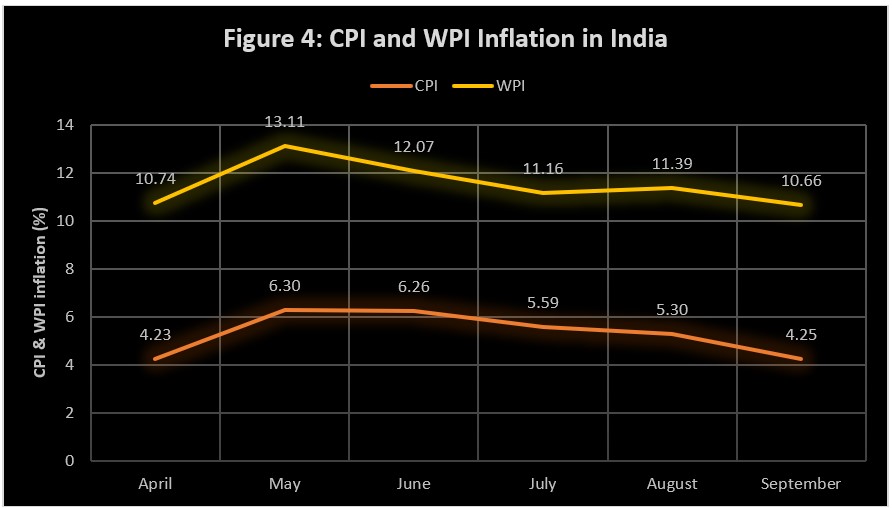

There continues to be a divergence between CPI and WPI inflation (Figure 4) because of the nature of the price indices and higher weighting of food items in CPI (47.25% against 15.26% for WPI) and that of manufactured items in WPI (64.23%).

Source: MOSPI, GoI and Office of the Economic Adviser, Ministry of Commerce and Industry, GoI

Bijetri Roy, Managing Director & Chief Strategy Officer, InsPIRE

Government of India (GoI), by announcing the Tata Group as the winning bidder for the sale of Air India on 8th October 2021, paved the way for the “Maharajah” to go back to the Tatas after seven decades. The bid was submitted by Tata Sons Pvt. Ltd. through its wholly owned subsidiary Talace Pvt. Ltd. At an enterprise value of INR 180 billion (USD 2.39 billion), the Tatas will get Air India, along with its low cost subsidiary Air India Express and a 50% stake in ground handling firm AISATS.

The Tatas will also get ownership of iconic brands like Air India, Indian Airlines, and the Maharajah, besides 141 aircraft and over 7,000 domestic and international airport slots. With the takeover of Air India, Tata Sons, which operates Vistara and AirAsia India, will become the second-largest airline in the domestic market with a market share of about 25%, and the largest Indian airline on international routes.

The bid value of INR 180 billion (USD 2.39 billion), includes INR 27 billion (USD 0.36 billion) to be paid by Tatas in cash for the acquisition, and INR 153 billion (USD 2.04 billion) debt that Tatas will take (to be retained in Air India). Further, Tatas will have to pay around INR 91.85 billion (USD 1.22 billion) towards capitalised lease obligation of 42 leased aircraft primarily the Boeing 787 Dreamliner aircraft.

This deal signifies the firm resolve of GoI to work towards strategic disinvestment, beginning with Air India, and to be followed by BPCL, Shipping Corporation of India, Container Corporation of India, IDBI Bank, BEML, Pawan Hans, Neelachal Ispat Nigam Limited, among others, to be completed in 2021-22, as announced in the Union Budget 2021-22. Privatisation of Air India has been a complex issue and it took two decades to fructify, while GoI has been suffering a daily loss of INR 200 million (USD 2.66 million) and an annual loss of INR 73 billion (USD 0.97 billion) for running Air India. The impact on GoI’s finances after the sale would be INR 446.78 billion (USD 5.95 billion).

The sale of Air India to the Tatas promises to transform the Indian aviation sector, strengthening competition in the domestic market and making Air India a major player in the international aviation market. At the same time, it places India on the right track on disinvestments and economic reforms agenda of the government.

The Reserve Bank of India (RBI) retained its accommodative stance and kept policy rates unchanged in its latest monetary policy announced on 8 October 2021. However, the beginning of normalisation of policy stance by halting its bond-buying efforts, was evident.

The six-member Monetary Policy Committee (MPC), headed by Governor Shaktikanta Das, unanimously decided to retain the policy repo rate at 4% and the reverse repo rate 3.35%. However, all members, except one, voted to continue with the accommodative stance as long as necessary to revive and sustain growth on a durable basis and mitigate the impact of Covid-19 on the economy, while ensuring that inflation remains within the target going forward. The Governor made it clear: “We do realise that as we approach the shore; when the shore is so close, we don’t want to rock the boat because we realise there is a life, there is a journey beyond the shore”.

However, the RBI decided to suspend the Government Securities Acquisition Programme (G-SAP), the Indian version of Quantitative Easing (QE) of the US. Through the G-SAP, RBI has injected INR 2.2 trillion (USD 29.3 billion) of liquidity in the system [out of the total INR 2.37 trillion (USD 31.5 billion) injected through bonds], during the first six months of 2021-22. The central bank would absorb a higher quantum of liquidity gradually through its 14-day variable rate reverse repo (VRRR) auctions, from the current INR 4 trillion (USD 53.2 billion) to INR 6 trillion (USD 79.9 billion) in stages, by December 2021.

The Governor justified the suspension of G-SAP by stating: “Given the existing liquidity overhang, the absence of a need for additional borrowing for GST compensation and the expected expansion of liquidity in the system as Government spending increases in line with budget estimates, the need for undertaking further G-SAP operations at this juncture does not arise. The Reserve Bank, however, would remain in readiness to undertake G-SAP as and when warranted by liquidity conditions and also continue to flexibly conduct other liquidity management operations including Operation Twist (OT) and regular open market operations (OMOs)”.

Deputy Governor Michael D. Patra explained that RBI is still in passive liquidity mode and was accepting what the market was offering, and that the central bank aims to move to an active mode of liquidity management.

The RBI sharply moderated the outlook for CPI inflation during 2021-22 from 5.7% projected in the previous MPC meeting (04-06 August 2021) to 5.3%, due to easing of food prices, combined with favourable base effects. However, prices of crude oil which will remain volatile over uncertainties on the global supply and demand conditions, rising metals and energy prices, acute shortage of key industrial components and high logistics costs are adding to input cost pressures. The inflation projection for Q2 FY2021-22 was reduced from 5.9% to 5.1%; and 5.3% to 4.5% in Q3. The inflation projection, however, remained the same at 5.8% for Q4. The risks continued to remain broadly balanced. The inflation projection for Q1 2022-23 was raised from 5.1% to 5.2%.

Projection for India’s GDP growth rate by the MPC was at 9.5%, which was same as the previous projection. Domestic economic activity is expanding with the weakening of the second covid wave. With favourable prospects for kharif and rabi crops, rural demand is expected to be buoyant. Significant increase in the pace of vaccination and the forthcoming festival season, are expected to support a rebound in the pent-up demand for contact intensive services, and boost growth. Easy monetary and financial conditions would also support growth. Further, the reforms undertaken by the government focusing on infrastructure development, asset monetisation, taxation, telecom sector and banking sector should push up investor confidence, enhance capacity expansion and facilitate crowding in of private investment. The production-linked incentive (PLI) scheme also augurs well for domestic manufacturing and exports.

However, downside risks to growth are global semiconductor shortages, elevated commodity prices and input costs, and potential global financial market volatility. Projection for Q2 GDP growth was raised from 7.3% in the previous MPC meeting to 7.9%. Q3 projection was retained at 6.3%, and 6.1% growth was retained for Q4. The real GDP growth for Q1 2022-23 was estimated at 17.2%, which is same as the previous projection.

Given the inflation expectations and growth projections for the current financial year, it is expected that the RBI would retain its accommodative stance at least till the MPC meeting in April 2022, while maintaining the policy repo rate at 4%. However, the next step for the central bank in liquidity management would be to raise the reverse repo rate from 3.35% to 3.50% in December 2021 and 3.75% in February 2022.

Government of India on 15 September 2021 announced a major relief package for telecom companies, overburdened with regulatory dues. The package would also attract the much needed foreign investment and encourage competition in the sector.

The announcement includes a major relief for the telecom operators by way of a four-year moratorium on adjusted gross revenue (AGR) dues, and the option for the government to convert dues into equity after the moratorium period expires. Also, non-telecom revenue will be removed from AGR.

It is also important that the government has taken the decision to protect government revenue by charging interest on the companies availing the moratorium. The interest rate charged will be marginal cost of funds based lending rate (MCLR) plus 2%., which is quite reasonable, and the penalty has been eliminated. The moratorium is expected to resolve the cash flow problem of the telecom companies, and also the improved cash flow can be utilised for investing in the upgradation of technology.

The relief package includes the following measures to give the much needed boost to the telecom sector:

100% FDI in the sector through the automatic route, with safeguards. Presently 100% FDI is allowed, but only 49% is in the automatic route.

About 80% reduction in bank guarantee requirements against licence fee and other similar levies.

Interest rates are to be rationalised, and penalties are to be removed with effect from 01 October 2021.

No bank guarantees will be required to secure instalment payments for future auctions.

In future auctions, tenure of spectrum has been increased from 20 to 30 years.

Spectrum usage charge (SUC) would not be levied for spectrum acquired in future auctions.

No additional SUC of 0.5% would be charges for spectrum sharing.