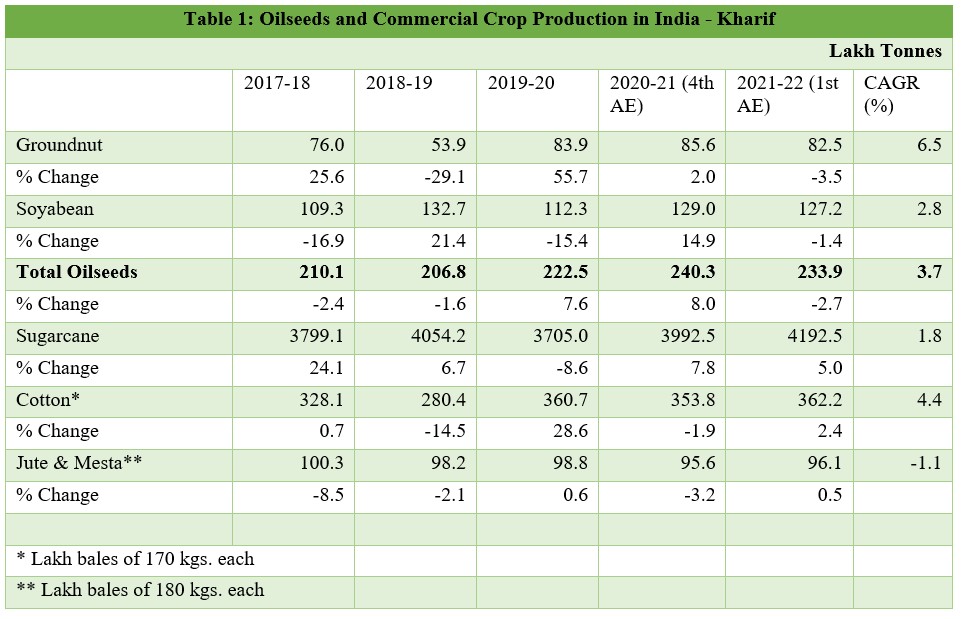

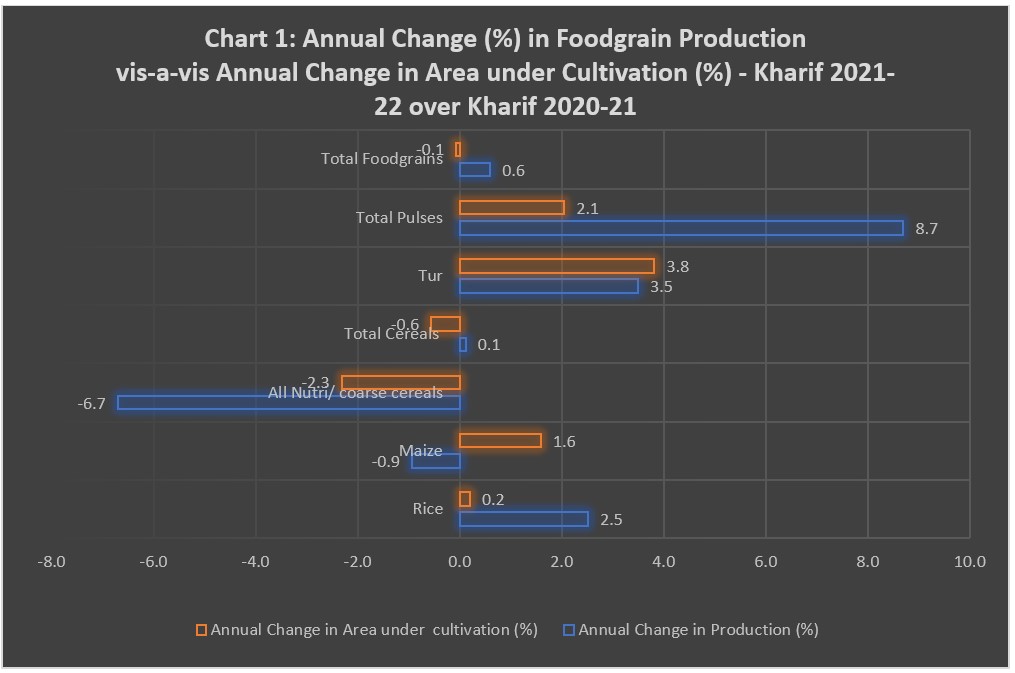

The estimated production of oilseeds is set to decline by -1.4% to 233.9 lakh tonnes (LT) in Kharif 2021-22, from 240.3 LT in 2020-21, due to a decline in acreage by -1.3% (Table 1 and Chart 1). The five-year CAGR of oilseeds production is estimated to be 3.7%. India’s demand for oilseeds is mostly met through imports. Therefore, Government of India’s decision to launch the National Mission on Edible Oils – Oil Palm (NMEO-OP), a Centrally Sponsored Scheme, is expected to significantly increase acreage and output of oilseeds in the country.

Among major oilseeds, groundnut and soyabean are expected to experience decline in output in kharif 2021-22. Groundnut output is estimated to decline by -3.5% to 82.5 LT, due to -3.6% decline in area under cultivation (Table 1 and Chart 1). The five-year CAGR of groundnut production is estimated to be 6.5%. It is estimated that soyabean production would decline by -1.4% to 127.2 LT, although there has been a marginal increase of 0.5% in acreage. Soyabean output would grow at a five-year CAGR of 2.8%.

Commercial crops like sugarcane and cotton are expected to perform better than the previous year. Sugarcane production is estimated to grow at 5% over the previous year to set a record of 4192.5 LT, on account of 1.6% increase in acreage. The output of cotton is expected to increase by 4.4% to 362.2 lakh bales, although there has been a significant decline of -5.8% in the area under cultivation, signifying an improvement in productivity. Finally, the output of Jute and Mesta is expected to decline by -1.1% to 96.1 lakh bales, although there has been an increase of 1% in acreage (Table 1 and Chart 1).

Source: First Advance Estimates of Production of Foodgrains for 2021-22, Ministry of Agriculture and Farmers’ Welfare, GoI, and calculations by InsPIRE.

Source: Prepared by InsPIRE, based on data accessed from First Advance Estimates of Production of Foodgrains for 2021-22, and Progress Report of Kharif Area Coverage as on 17/09/2021, Ministry of Agriculture and Farmers’ Welfare, GoI.

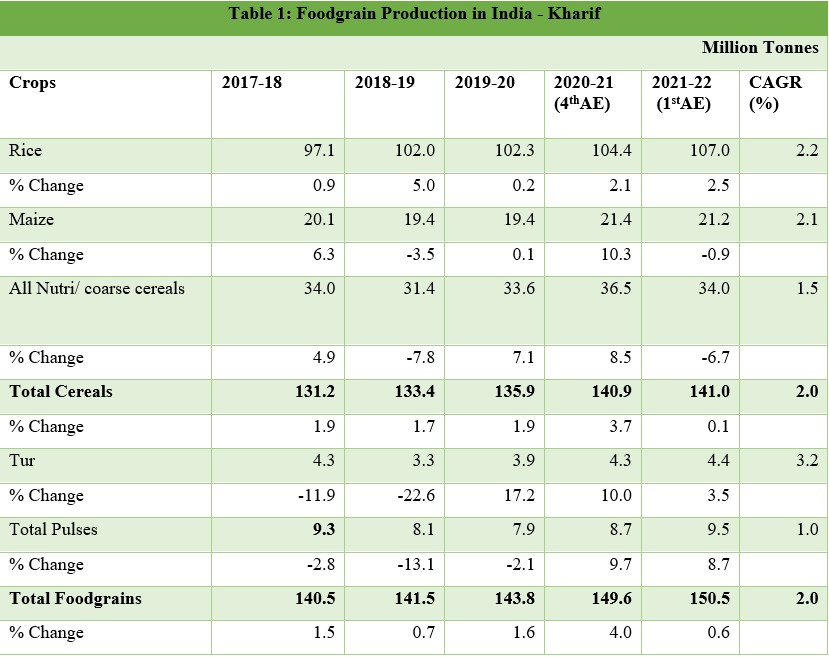

India’s foodgrain production for the kharif season 2021-22 is estimated to reach a record 150.5 million tonnes (0.6% increase over 2020-21, albeit a decline in acreage of -0.1%), while growing at a five-year CAGR of 2% (Table 1 and Chart 1). This was mainly on account of increased area under cultivation of rice and pulses (mainly tur or arhar). The estimated increase in acreage under these crops was facilitated by a surge in monsoon rains in September 2021.

The output of kharif rice is estimated to touch a record 107 million tonnes (MT), registering a growth of 2.5% over the previous year (Table 1). However, the area under cultivation of rice has increased marginally by 0.2% over 2020-21 (Chart 1), signifying efficiency gains in the cultivation of the crop. During the last five years, the production of kharif rice has grown at a CAGR of 2.2% (Table 1). Maize, with an estimated output of 21.2 MT, has experienced -0.9% annual change in production, against a 1.6% increase in area, signifying a decline in yield. The five-year CAGR of maize output stood at 2.1%. Nutri/ coarse cereals as a whole have witnessed significant decline in the estimated output by -6.7% and acreage by -2.3%.

While the estimated output of tur (4.4 MT) increased by 3.5%, acreage increased by 3.8%. The production during the last five years increased by an impressive CAGR of 3.2%. The estimated output of pulses as a whole (9.5MT), increased significantly by 8.7% over the previous year, while the acreage had increased by 2.1% (Chart 1), indicating an increase in yield, The five-year CAGR of pulses stood at 1% (Table 1).

Source: First Advance Estimates of Production of Foodgrains for 2021-22, Ministry of Agriculture and Farmers’ Welfare, GoI, and calculations by InsPIRE.

Source: Prepared by InsPIRE, based on data accessed from First Advance Estimates of Production of Foodgrains for 2021-22, and Progress Report of Kharif Area Coverage as on 17/09/2021, Ministry of Agriculture and Farmers’ Welfare, GoI.

Bijetri Roy, Managing Director & Chief Strategy Officer, InsPIRE

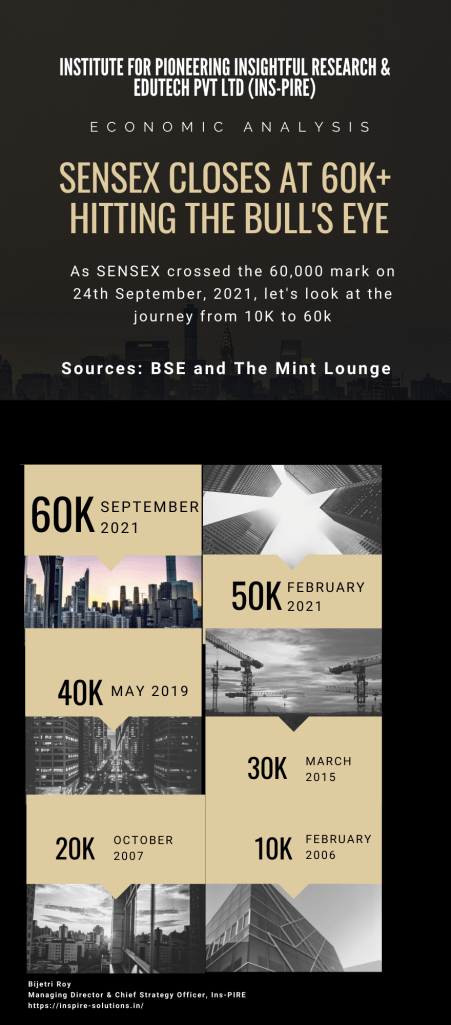

SENSEX closed at 60,048.47 on 24th September, 2021, ear-marking a high in the graphs, since the last milestone of 50,255.75 on 3rd February, 2021. In fact, even the BSE Realty and NIFTY IT indices closed at their respective highs of 4002.46 and 37,103.25.

This is a clear indication that India is still the flavour of the season, despite a probable slowdown in China or smaller bond purchase by central banks.

Earlier this week, Sanjeev Prasad, Kotak Institutional Equities said, “We expect a strong economic and earnings revival and a stable COVID-19 situation to provide short-term support to the market. We do not see any change to India’s medium-term narratives, including favourable demographics and likely multi-year investment cycle led by corporate and household capital expenditure.” (Source: Financial Express)

In the last four seasons, Domestic Institutional Investors (DIIs) invested in shares worth USD 1 billion, while Foreign Portfolio Investors (FPIs) invested in Indian equity worth USD 9 billion. (Source: Financial Express)

According to Piyush Garg, Chief Investment Officer at ICICI Securities Ltd, “Indian stocks have been performing well over the past few quarters due to robust liquidty, upward earnings cucle and an economic revival led by a fading pandemic. (Source: Mint Lounge)

Infographic designed by Institute for Pioneering Insightful Research & Edutech Pvt Ltd (InsPIRE)

“SENSEX reaching 60,000 shows India’s growth potential and its emergence as a world leader, amid Covid”, Ashish Chauhan, MD & CEO, BSE.

However, looking at the global markets at present, investors should be cautious of the following:

Rising inflation

Subsequent squeeze in liquidity

Overall, India is definitely the flavour of the season, having hit the “bull’s” eye with the 60K milestone.

The Union Finance Minister Ms. Nirmala Sitharaman on 16 September 2021 announced that the Reconstruction Company Ltd (NARCL) would be operational soon. The NARCL would ensure resolving bad loans within five years, beyond which the guarantee to be issued by the government would expire.

The Union Cabinet had on 15 September 2021 approved a government guarantee of INR 306 billion (USD 4.15 billion) to be provided for the security receipts issued by the NARCL to buy bad loans of banks. The FM has stated that in many cases, the guarantee need not be invoked as it is reasonable to expect that realization in many cases will be more than the acquisition cost.

The NARCL would acquire assets by making an offer to the lead bank. Once the offer is accepted, India Debt Resolution Company (IDRC), in which PSBs will hold up to 49% stake, will be engaged for management and value addition. The NARCL would resolve stressed loans above INR 5 billion (USD 0.07 billion) each, amounting to about INR 2 trillion (USD 21.14 billion) in phases.

These stressed assets would be acquired by NARCL by paying 15% cash to lenders and the remaining 85% would be paid through security receipts, backed by government guarantee. These security receipts will be tradeable. Fully provisioned assets of INR900 billion are to be transferred to NARCL in the first phase. The new framework will facilitate the freeing up of banking personnel to focus on increasing business and credit growth.

A government guarantee can be invoked to cover the shortfall between the amount realised from the underlying assets and the face value of the security receipts issued for such assets, subject to an overall ceiling of INR 306 billion (USD 4.15 billion). The condition for invoking the guarantee will be either resolution or liquidation.

A major concern is that a proper market for impaired assets is yet to develop in India. However, the new mechanism could allow market-driven payment flexibility by adopting newly-devised auction formats.

A PLI scheme for the automotive industry in India was announced by the Union Cabinet on 15September 2021. With a budgetary outlay of INR 259.38 billion (USD 3.52 bn), the scheme aims to boost domestic manufacturing capabilities of the automobile industry, including electric and hydrogen fuel cell vehicles. The incentives to the automobile industry would be provided over a period of five years.

Last year, the government had announced a PLI scheme for the auto-component sector with an outlay of INR 570.43 billion (USD 7.74 billion). However, the allocation has been slashed by more than 50%, in view of the government’s priority to green automotive manufacturing. Nevertheless, both the schemes, together, promises to reinvigorate the automobile industry, to make it export competitive. The new PLI scheme is expected to be a game changer by incentivising both existing automakers and non-automotive investors to mainstream the manufacturing of green vehicles in the world’s fifth largest automotive market.

The new scheme aims to incentivise high-value advanced automotive technology vehicles and products such as sunroofs, adaptive front lighting, automatic braking, tyre pressure monitoring system, and collision warning systems, etc. The government has stated: “The incentive structure will encourage industry to make fresh investments for indigenous global supply chains of advanced automotive technology products.”

The government has further stated that, the existing INR181billion (USD 2.46 billion) scheme for advanced chemistry cell as well as the INR 100 billion (USD 1.35 billion). Faster Adoption of Manufacturing of Electric Vehicles (FAME) scheme would enable India to leapfrog from traditional fossil fuel-based transportation system to greener, sustainable, advanced and more efficient EV-based system. Presently, the share of advanced automotive technology in the Indian automobile sector is at 3%, as against 18% globally. The government has also clarified that components of internal combustion engine (ICE) vehicles that are not made in India will be incentivized, apart from incentivising the manufacture of electric vehicles (EVs) and hydrogen fuel cell vehicles.

The government has estimated that the PLI scheme for the auto sector will attract fresh investments of over INR 425 billion (USD 5.77 billion) and incremental production of over INR 2.3 trillion (USD 31.21 billion), over a period of five years. Further, additional employment opportunities for over 750,000 people are estimated to be created. The scheme is expected to accelerate India’s share in global automotive trade.

The new PLI scheme is open to existing automotive companies as well as new investors, who are from the non-automotive industry. The two components of the scheme are: the champion Original Equipment Manufacturers (OEM) incentive scheme and the component champion incentive scheme. The OEM incentive scheme is a ‘sales value-linked’ scheme, applicable to EVs and hydrogen fuel cell vehicles across all segments.

To avail the scheme, the OEMs must have a minimum of INR100 billion (USD 1.35 billion) in revenue and will have to make new investments of INR 20 billion (USD 0.27 billion) in five years to take benefits from the scheme. For two-wheeler companies, the amount of new investment is INR10 billion (USD 0.14 billion). Auto-component makers must have a minimum revenue of INR 5 billion (USD 0.07 billion) and INR1.50 billion (USD 0.2 billion) fixed assets investment to be eligible for the PLI. Non-automotive investors must have a global net worth of INR 10 billion (USD 0.14 billion) and a clear business plan for investment in advanced automotive technologies to be eligible for the scheme.

India’s retail inflation, measured by the Consumer Price Index (CPI), cooled down for the second consecutive month to 5.3% in August 2021, from 5.6% in the previous month (Figure 1), thereby moving further below the Reserve Bank of India’s (RBI) upper tolerance limit of 6% inflation. This gives credence to RBI’s view about the transient nature of the elevated level of inflation, driven by “exogenous and largely temporary supply shocks” during Covid times, justifying the continued accommodative monetary policy stance of the central bank for supporting growth.

During the last six months inflation remained above RBI’s medium-term target of 4%, and even exceeded the upper tolerance limit of 6% in May and June, at 6.3% each, on account of high food and fuel prices. Both rural and urban inflation also remained in the range of 6.0%-6.6% during these two months, before sliding down to below 6.0% in July and August.

Source: MOSPI, GoI

The principal reason behind the decline in retail inflation in August is the easing of food inflation (Figure 2). The Consumer Food Price Inflation (CFPI) declined steadily from 5.2% in June 2021 to 4.0% in July 2021and 3.1% in August 2021. Food inflation fell as vegetable, cereal and sugar inflation declined by 11.7%, 1.2% and 0.6%, respectively, during the month, though inflation for protein items such as edible oils (33%), pulses (8.8%), eggs (16.3%) and meat and fish (9.2%) remained elevated.

Fuel inflation (12.95%) increased and services inflation also remained high at 6.4% in August. Core inflation excluding food and fuel prices rose by a slower 5.5% in August against 5.7% in July.

Source: MOSPI, GoI

Favourable base effect, along with further easing of food inflation in the coming months due to possible good kharif harvest, will enable inflation to remain benign. This would give enough leeway to the RBI to continue with the accommodative stance, at least till February 2021 monetary policy review. However, inflation risks remain high due to elevated international commodity prices, including crude oil prices. Further, price pressures could intensify due to the second-round effects of high fuel costs, resulting in higher prices of other goods, after a time lag. Although core CPI inflation declined by 20 bps, it remained elevated despite the presence of excess capacity. Services inflation is another potential source of upward pressure on inflation, as consumption expenditure will rise during the upcoming festive season.

RBI in the last review of the monetary policy (04-06 August 2021) had raised the inflation forecast for FY 2022 to an average of 5.7% from the earlier forecast of 5.1%. It is further expected that the central bank could, given the latest inflation print and inflation expectations, revise the inflation estimate downwards for the full fiscal year. The September edition of RBI Bulletin, states that the softening prices of various food items was likely to extend into Q3 of FY22, which will, in effect, contain the upward pressure from fuel and core prices on headline inflation. The next monetary policy review in October 2021 would, therefore, in all likelihood maintain an accommodative stance, for the eighth time in a row, with a greater focus on liquidity management via absorption measures.

Wholesale Inflation

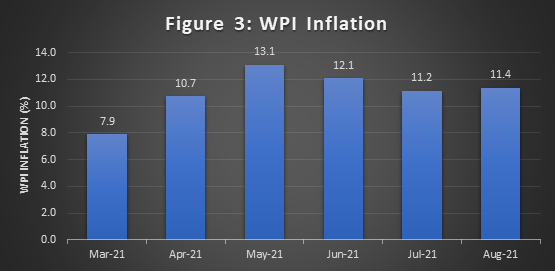

India’s WPI inflation rose marginally to 11.4% in August 2021 after declining from 13.1% in May, 12.1% in June and 11.2% in July (Figure 3). The elevated WPI inflation was on account of high inflation of manufactured products (weight of 64.2%) in May, June, July and August at 11.3%, 11.0%, 11.2% and 11.4%, respectively.

It is evident that cost push pressures are gradually seeping into prices of manufactured goods. The highest inflation was observed in case of crude petroleum and natural gas at 59.5%, 47.0%, 40.3% and 40.0%, respectively, during the last four months. Fuel and power inflation at 36.7%, 29.3%, 26.0% and 26.1%, respectively in May, June, July and August. However, food inflation contracted by 1.29% in August.

Price volatility in the international markets for crude oil and rising prices of edible oils and metal products would lead to further rise in WPI inflation, considering the fact that India is a price taker for most of these commodities.

Source: Office of the Economic Adviser, Ministry of Commerce and Industry, GoI

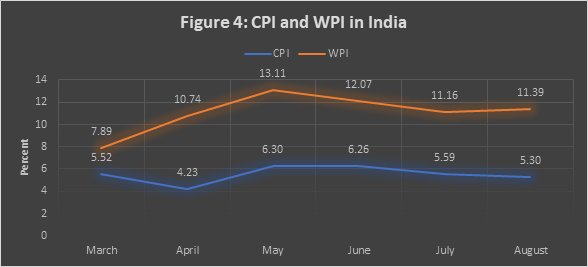

There continues to be a divergence between CPI and WPI inflation (Figure 4) because of the nature of the price indices and higher weighting of food items in CPI (47.25% against 15.26% for WPI) and that of manufactured items in WPI (64.23%).

Source: MOSPI, GoI and Office of the Economic Adviser, Ministry of Commerce and Industry, GoI