Dr Debesh Roy, Chairman, InsPIRE

Retail Inflation

India’s retail inflation, measured by the Consumer Price Index (CPI), cooled down for the second consecutive month to 5.3% in August 2021, from 5.6% in the previous month (Figure 1), thereby moving further below the Reserve Bank of India’s (RBI) upper tolerance limit of 6% inflation. This gives credence to RBI’s view about the transient nature of the elevated level of inflation, driven by “exogenous and largely temporary supply shocks” during Covid times, justifying the continued accommodative monetary policy stance of the central bank for supporting growth.

During the last six months inflation remained above RBI’s medium-term target of 4%, and even exceeded the upper tolerance limit of 6% in May and June, at 6.3% each, on account of high food and fuel prices. Both rural and urban inflation also remained in the range of 6.0%-6.6% during these two months, before sliding down to below 6.0% in July and August.

The principal reason behind the decline in retail inflation in August is the easing of food inflation (Figure 2). The Consumer Food Price Inflation (CFPI) declined steadily from 5.2% in June 2021 to 4.0% in July 2021and 3.1% in August 2021. Food inflation fell as vegetable, cereal and sugar inflation declined by 11.7%, 1.2% and 0.6%, respectively, during the month, though inflation for protein items such as edible oils (33%), pulses (8.8%), eggs (16.3%) and meat and fish (9.2%) remained elevated.

Fuel inflation (12.95%) increased and services inflation also remained high at 6.4% in August. Core inflation excluding food and fuel prices rose by a slower 5.5% in August against 5.7% in July.

Favourable base effect, along with further easing of food inflation in the coming months due to possible good kharif harvest, will enable inflation to remain benign. This would give enough leeway to the RBI to continue with the accommodative stance, at least till February 2021 monetary policy review. However, inflation risks remain high due to elevated international commodity prices, including crude oil prices. Further, price pressures could intensify due to the second-round effects of high fuel costs, resulting in higher prices of other goods, after a time lag. Although core CPI inflation declined by 20 bps, it remained elevated despite the presence of excess capacity. Services inflation is another potential source of upward pressure on inflation, as consumption expenditure will rise during the upcoming festive season.

RBI in the last review of the monetary policy (04-06 August 2021) had raised the inflation forecast for FY 2022 to an average of 5.7% from the earlier forecast of 5.1%. It is further expected that the central bank could, given the latest inflation print and inflation expectations, revise the inflation estimate downwards for the full fiscal year. The September edition of RBI Bulletin, states that the softening prices of various food items was likely to extend into Q3 of FY22, which will, in effect, contain the upward pressure from fuel and core prices on headline inflation. The next monetary policy review in October 2021 would, therefore, in all likelihood maintain an accommodative stance, for the eighth time in a row, with a greater focus on liquidity management via absorption measures.

Wholesale Inflation

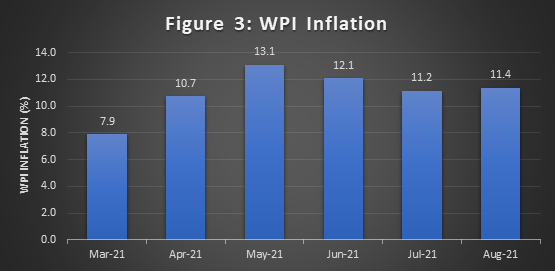

India’s WPI inflation rose marginally to 11.4% in August 2021 after declining from 13.1% in May, 12.1% in June and 11.2% in July (Figure 3). The elevated WPI inflation was on account of high inflation of manufactured products (weight of 64.2%) in May, June, July and August at 11.3%, 11.0%, 11.2% and 11.4%, respectively.

It is evident that cost push pressures are gradually seeping into prices of manufactured goods. The highest inflation was observed in case of crude petroleum and natural gas at 59.5%, 47.0%, 40.3% and 40.0%, respectively, during the last four months. Fuel and power inflation at 36.7%, 29.3%, 26.0% and 26.1%, respectively in May, June, July and August. However, food inflation contracted by 1.29% in August.

Price volatility in the international markets for crude oil and rising prices of edible oils and metal products would lead to further rise in WPI inflation, considering the fact that India is a price taker for most of these commodities.

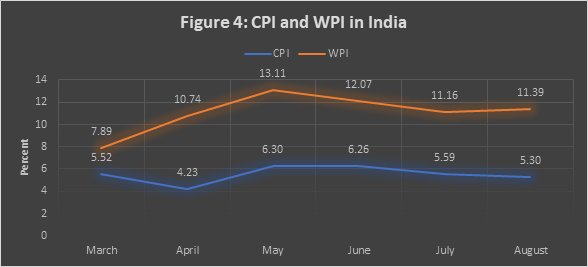

There continues to be a divergence between CPI and WPI inflation (Figure 4) because of the nature of the price indices and higher weighting of food items in CPI (47.25% against 15.26% for WPI) and that of manufactured items in WPI (64.23%).