Government of India on 15 September 2021 announced a major relief package for telecom companies, overburdened with regulatory dues. The package would also attract the much needed foreign investment and encourage competition in the sector.

The announcement includes a major relief for the telecom operators by way of a four-year moratorium on adjusted gross revenue (AGR) dues, and the option for the government to convert dues into equity after the moratorium period expires. Also, non-telecom revenue will be removed from AGR.

It is also important that the government has taken the decision to protect government revenue by charging interest on the companies availing the moratorium. The interest rate charged will be marginal cost of funds based lending rate (MCLR) plus 2%., which is quite reasonable, and the penalty has been eliminated. The moratorium is expected to resolve the cash flow problem of the telecom companies, and also the improved cash flow can be utilised for investing in the upgradation of technology.

The relief package includes the following measures to give the much needed boost to the telecom sector:

100% FDI in the sector through the automatic route, with safeguards. Presently 100% FDI is allowed, but only 49% is in the automatic route.

About 80% reduction in bank guarantee requirements against licence fee and other similar levies.

Interest rates are to be rationalised, and penalties are to be removed with effect from 01 October 2021.

No bank guarantees will be required to secure instalment payments for future auctions.

In future auctions, tenure of spectrum has been increased from 20 to 30 years.

Spectrum usage charge (SUC) would not be levied for spectrum acquired in future auctions.

No additional SUC of 0.5% would be charges for spectrum sharing.

The Union Finance Minister Ms. Nirmala Sitharaman on 16 September 2021 announced that the Reconstruction Company Ltd (NARCL) would be operational soon. The NARCL would ensure resolving bad loans within five years, beyond which the guarantee to be issued by the government would expire.

The Union Cabinet had on 15 September 2021 approved a government guarantee of INR 306 billion (USD 4.15 billion) to be provided for the security receipts issued by the NARCL to buy bad loans of banks. The FM has stated that in many cases, the guarantee need not be invoked as it is reasonable to expect that realization in many cases will be more than the acquisition cost.

The NARCL would acquire assets by making an offer to the lead bank. Once the offer is accepted, India Debt Resolution Company (IDRC), in which PSBs will hold up to 49% stake, will be engaged for management and value addition. The NARCL would resolve stressed loans above INR 5 billion (USD 0.07 billion) each, amounting to about INR 2 trillion (USD 21.14 billion) in phases.

These stressed assets would be acquired by NARCL by paying 15% cash to lenders and the remaining 85% would be paid through security receipts, backed by government guarantee. These security receipts will be tradeable. Fully provisioned assets of INR900 billion are to be transferred to NARCL in the first phase. The new framework will facilitate the freeing up of banking personnel to focus on increasing business and credit growth.

A government guarantee can be invoked to cover the shortfall between the amount realised from the underlying assets and the face value of the security receipts issued for such assets, subject to an overall ceiling of INR 306 billion (USD 4.15 billion). The condition for invoking the guarantee will be either resolution or liquidation.

A major concern is that a proper market for impaired assets is yet to develop in India. However, the new mechanism could allow market-driven payment flexibility by adopting newly-devised auction formats.

A PLI scheme for the automotive industry in India was announced by the Union Cabinet on 15September 2021. With a budgetary outlay of INR 259.38 billion (USD 3.52 bn), the scheme aims to boost domestic manufacturing capabilities of the automobile industry, including electric and hydrogen fuel cell vehicles. The incentives to the automobile industry would be provided over a period of five years.

Last year, the government had announced a PLI scheme for the auto-component sector with an outlay of INR 570.43 billion (USD 7.74 billion). However, the allocation has been slashed by more than 50%, in view of the government’s priority to green automotive manufacturing. Nevertheless, both the schemes, together, promises to reinvigorate the automobile industry, to make it export competitive. The new PLI scheme is expected to be a game changer by incentivising both existing automakers and non-automotive investors to mainstream the manufacturing of green vehicles in the world’s fifth largest automotive market.

The new scheme aims to incentivise high-value advanced automotive technology vehicles and products such as sunroofs, adaptive front lighting, automatic braking, tyre pressure monitoring system, and collision warning systems, etc. The government has stated: “The incentive structure will encourage industry to make fresh investments for indigenous global supply chains of advanced automotive technology products.”

The government has further stated that, the existing INR181billion (USD 2.46 billion) scheme for advanced chemistry cell as well as the INR 100 billion (USD 1.35 billion). Faster Adoption of Manufacturing of Electric Vehicles (FAME) scheme would enable India to leapfrog from traditional fossil fuel-based transportation system to greener, sustainable, advanced and more efficient EV-based system. Presently, the share of advanced automotive technology in the Indian automobile sector is at 3%, as against 18% globally. The government has also clarified that components of internal combustion engine (ICE) vehicles that are not made in India will be incentivized, apart from incentivising the manufacture of electric vehicles (EVs) and hydrogen fuel cell vehicles.

The government has estimated that the PLI scheme for the auto sector will attract fresh investments of over INR 425 billion (USD 5.77 billion) and incremental production of over INR 2.3 trillion (USD 31.21 billion), over a period of five years. Further, additional employment opportunities for over 750,000 people are estimated to be created. The scheme is expected to accelerate India’s share in global automotive trade.

The new PLI scheme is open to existing automotive companies as well as new investors, who are from the non-automotive industry. The two components of the scheme are: the champion Original Equipment Manufacturers (OEM) incentive scheme and the component champion incentive scheme. The OEM incentive scheme is a ‘sales value-linked’ scheme, applicable to EVs and hydrogen fuel cell vehicles across all segments.

To avail the scheme, the OEMs must have a minimum of INR100 billion (USD 1.35 billion) in revenue and will have to make new investments of INR 20 billion (USD 0.27 billion) in five years to take benefits from the scheme. For two-wheeler companies, the amount of new investment is INR10 billion (USD 0.14 billion). Auto-component makers must have a minimum revenue of INR 5 billion (USD 0.07 billion) and INR1.50 billion (USD 0.2 billion) fixed assets investment to be eligible for the PLI. Non-automotive investors must have a global net worth of INR 10 billion (USD 0.14 billion) and a clear business plan for investment in advanced automotive technologies to be eligible for the scheme.

India’s retail inflation, measured by the Consumer Price Index (CPI), cooled down for the second consecutive month to 5.3% in August 2021, from 5.6% in the previous month (Figure 1), thereby moving further below the Reserve Bank of India’s (RBI) upper tolerance limit of 6% inflation. This gives credence to RBI’s view about the transient nature of the elevated level of inflation, driven by “exogenous and largely temporary supply shocks” during Covid times, justifying the continued accommodative monetary policy stance of the central bank for supporting growth.

During the last six months inflation remained above RBI’s medium-term target of 4%, and even exceeded the upper tolerance limit of 6% in May and June, at 6.3% each, on account of high food and fuel prices. Both rural and urban inflation also remained in the range of 6.0%-6.6% during these two months, before sliding down to below 6.0% in July and August.

Source: MOSPI, GoI

The principal reason behind the decline in retail inflation in August is the easing of food inflation (Figure 2). The Consumer Food Price Inflation (CFPI) declined steadily from 5.2% in June 2021 to 4.0% in July 2021and 3.1% in August 2021. Food inflation fell as vegetable, cereal and sugar inflation declined by 11.7%, 1.2% and 0.6%, respectively, during the month, though inflation for protein items such as edible oils (33%), pulses (8.8%), eggs (16.3%) and meat and fish (9.2%) remained elevated.

Fuel inflation (12.95%) increased and services inflation also remained high at 6.4% in August. Core inflation excluding food and fuel prices rose by a slower 5.5% in August against 5.7% in July.

Source: MOSPI, GoI

Favourable base effect, along with further easing of food inflation in the coming months due to possible good kharif harvest, will enable inflation to remain benign. This would give enough leeway to the RBI to continue with the accommodative stance, at least till February 2021 monetary policy review. However, inflation risks remain high due to elevated international commodity prices, including crude oil prices. Further, price pressures could intensify due to the second-round effects of high fuel costs, resulting in higher prices of other goods, after a time lag. Although core CPI inflation declined by 20 bps, it remained elevated despite the presence of excess capacity. Services inflation is another potential source of upward pressure on inflation, as consumption expenditure will rise during the upcoming festive season.

RBI in the last review of the monetary policy (04-06 August 2021) had raised the inflation forecast for FY 2022 to an average of 5.7% from the earlier forecast of 5.1%. It is further expected that the central bank could, given the latest inflation print and inflation expectations, revise the inflation estimate downwards for the full fiscal year. The September edition of RBI Bulletin, states that the softening prices of various food items was likely to extend into Q3 of FY22, which will, in effect, contain the upward pressure from fuel and core prices on headline inflation. The next monetary policy review in October 2021 would, therefore, in all likelihood maintain an accommodative stance, for the eighth time in a row, with a greater focus on liquidity management via absorption measures.

Wholesale Inflation

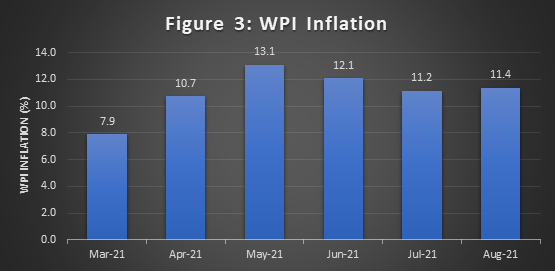

India’s WPI inflation rose marginally to 11.4% in August 2021 after declining from 13.1% in May, 12.1% in June and 11.2% in July (Figure 3). The elevated WPI inflation was on account of high inflation of manufactured products (weight of 64.2%) in May, June, July and August at 11.3%, 11.0%, 11.2% and 11.4%, respectively.

It is evident that cost push pressures are gradually seeping into prices of manufactured goods. The highest inflation was observed in case of crude petroleum and natural gas at 59.5%, 47.0%, 40.3% and 40.0%, respectively, during the last four months. Fuel and power inflation at 36.7%, 29.3%, 26.0% and 26.1%, respectively in May, June, July and August. However, food inflation contracted by 1.29% in August.

Price volatility in the international markets for crude oil and rising prices of edible oils and metal products would lead to further rise in WPI inflation, considering the fact that India is a price taker for most of these commodities.

Source: Office of the Economic Adviser, Ministry of Commerce and Industry, GoI

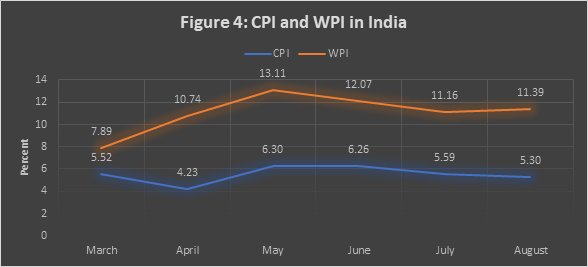

There continues to be a divergence between CPI and WPI inflation (Figure 4) because of the nature of the price indices and higher weighting of food items in CPI (47.25% against 15.26% for WPI) and that of manufactured items in WPI (64.23%).

Source: MOSPI, GoI and Office of the Economic Adviser, Ministry of Commerce and Industry, GoI