Dr Debesh Roy, Chairman, InsPIRE

The Federal Open Market Committee (FOMC) at its meeting held on 22 September 2021, unanimously decided to maintain the rate of interest paid on reserve balances at 0.15% and also to continue with the federal funds rate in a target range of 0-0.25%, continuing with the accommodative stance. While the FOMC decided for now to continue with quantitative easing (QE) of $120 bn-a-month asset purchase program, the Fed Chair Mr. Jerome Powell made it amply clear that “tapering” of the program could be initiated at the next FOMC meeting in November 2021.

The stimulus package was introduced at the onset of the pandemic, and the US Federal Reserve pledged to maintain it until there was substantial progress on its dual goals of average 2% inflation and maximum employment. The Fed believes that the US economy would be on a firm footing on these two counts, and would, therefore start the tapering exercise. Mr. Powell also revealed that the FOMC broadly supports a gradual tapering and intends to withdraw the stimulus entirely around the second half of 2022.

There is however, less unanimity among Fed members regarding tightening of interest rates, as the eighteen-member Committee is now evenly split on the prospects of a rate increase in 2022. There could be three rate hikes by the end of 2023.

Impact of Taper Decision by US Fed on Emerging Market and Developing Economies (EMDEs) like India

Financial markets globally, including India’s seem to have factored in the imminent gradual tapering exercise by the US Federal Reserve. Indian markets continued to surge, in spite of the almost certain tapering from November 2021. QEs with near zero interest rates in developed countries, led to massive flow of funds to emerging market economies.

The 2013 tapering by US Fed in the aftermath of the Global Financial Crisis, led to what is known as “taper tantrum”. In response to the statement by the then Fed Chair Dr. Ben Bernanke in May 2013, suggesting that the FOMC might soon start to slow down its bond purchases, the US 10-year bond yield surged and triggered a wave of capital flight from emerging economies. The countries affected the most from the “taper tantrum” were South Africa, Brazil, India, Indonesia and Turkey, which were dubbed the “fragile five” by Morgan Stanley due to their high current account deficits and dependence on inflows of foreign capital.

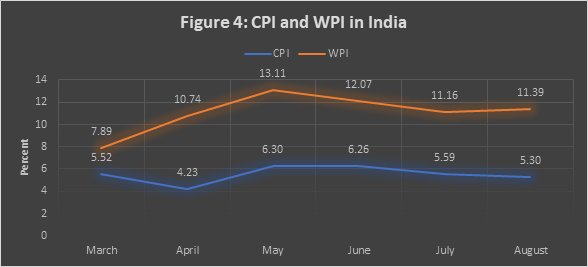

However, the situation is vastly different now, and “taper tantrum” can be ruled out in India. Foreign Institutional Investors (FIIs) have invested $8.94 billion in India so far in 2021. The Sensex and Nifty have gained 23-25% during the year. The effect of the tapering would be relatively low for India’s markets due to strong fundamentals, with a low current account deficit and a high and steadily growing foreign exchange reserves, which have touched a comfortable $640 billion (as on 17 September 2021). While high inflation is a problem, it is transient in nature, as underscored by the Reserve Bank of India.

The EMDEs must certainly remain vigilant and take necessary monetary and fiscal measures to prevent taper to turn into a “tantrum” to cause any major outflow of liquidity from these economies.