Dr. Debesh Roy, Chairman, InsPIRE

Introduction

The global economy is hamstrung with rising inflation and slowing growth. Inflation is now well-entrenched across the world, and is definitely not transitory in nature, as thought by US Fed Chair Mr. Jerome Powell and several economists, few months ago. The US consumer inflation surged ahead to touch a more than four decades high of 8.6% annual rate in May 2022, due to spiraling energy and food prices. Similarly, inflation in the UK touched a 40-year high of 9% in April, and is expected to touch 9.1% in May. Further six member states of the EU have inflation rates above 10%, and the average is 8.1%. Most developing countries have been suffering from the wrath of inflation and slowdown in economic growth. Inflation in developed as well as developing economies has been sparked by low interest rates and government stimulus to counter the Covid-19 pandemic’s impact, and disruption in global supply chains, followed by elevated energy and commodity prices due to the Russia-Ukraine crisis.

India has been witnessing rise in retail inflation above the Reserve Bank of India’s (RBI) mandated tolerance level of 6%, from January 2022. Wholesale inflation, however, started rising alarmingly from March 2021, onwards. The RBI and Government of India (GoI) have initiated monetary and fiscal measures, respectively, to curb inflation.

Easing of India’s Retail Inflation

India’s retail [Consumer Price Index (CPI)] inflation eased in May 2022 to 7.04% from an almost eight years high of 7.79% in April (Figure 1). However, it remained above RBI’s upper tolerance level of 6% for the fifth month in a row. There was a broad-based deceleration in inflation, mainly on account of slower increases in food prices. Core inflation, too, moderated in May to 6.09% from 6.96% in the previous month.

The slowing down of inflation was mainly on account of deceleration in rural CPI inflation, which declined significantly from 8.38% in April 2022 to 7.01% in May (Figure 1), as a result of a decline in the combined weighted contribution of health, education and personal care and effects by 35 basis points (bps), and 40 bps decline in the weighted contribution of food and beverages. Urban inflation, however, declined marginally from 7.09% in April to 7.08% in May (Figure 1). Favourable base effect, too contributed to the decline in inflation. However, there are more upside risks to inflation, with international crude oil prices remaining stubbornly high.

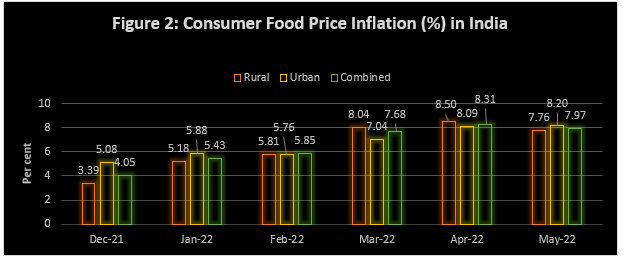

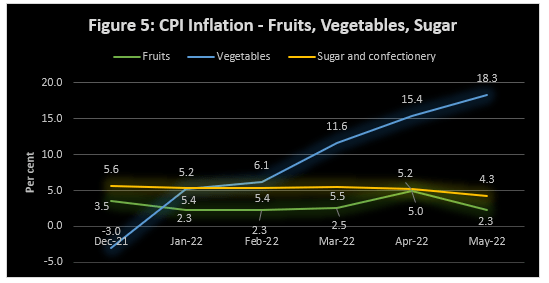

The consumer food price inflation (CFPI) is the major determinant of retail inflation in India, with a weightage of 39.1% in the CPI. During the six-month period December 2021 to May 2022, CFPI more than doubled from 4.05% in December to 8.31% in April, before dropping to 7.97% in May (Figure 2). This was due to elevated oils and fats inflation at 24.3% in December to 13.3% in May (Figure 3) and a sharp increase in vegetable inflation from -3% in December to 18.3% in May (Figure 5). India imports nearly 60% of its crude edible oil requirement. Around 90% of India’s annual crude sunflower oil requirement of 22-23 lakh tonne is imported from Ukraine to the tune of 70% and 20% from Russia and the remaining 10% from Argentina. The Ukraine-Russia conflict has disrupted supplies of sunflower oil and sharply pushed up its price in the international market, impacting India’s import cost.

The principal reason for a sharp rise in vegetable prices is the increase in transportation cost due to high fuel price, which in turn is the result of elevated international price of crude oil. High tomato prices, due to fall in production on account of heatwaves prevailing in different parts of the country, also impacted vegetable inflation.

While cereal inflation increased steadily from 2.6 % in December 2021 to 5,3% in May 2022, pulses inflation declined from 2.4% to -0.4% during the same period (Figure 3). Decline in pulses inflation was on account of record estimated production of pulses in the Kharif and Rabi seasons in the year 2021-22, as well as higher imports of Arhar and Urad.

Inflation in eggs declined sharply from 4.2% in February to -4.6% in May (Figure 4). Meat and fish inflation rose to 8.2% in May from 7% in the previous month, before falling from 9.6% in March, while milk inflation increased steadily from 3.8% in December 2021 to 5.6% in May 2022 (Figure 4).

Fruit inflation declined sharply from 5% in April to 2.3% in May, while sugar inflation fell from 5.2% to 4.3% (Figure 5).

Fuel and light inflation remained elevated during the period at 11% in December 2021, 10.8% in April 2022 and 9.5% in May 2022 (Figure 6), on account of high international crude oil prices, with Brent crude prices remaining around $120 per barrel.

Surging Wholesale Inflation

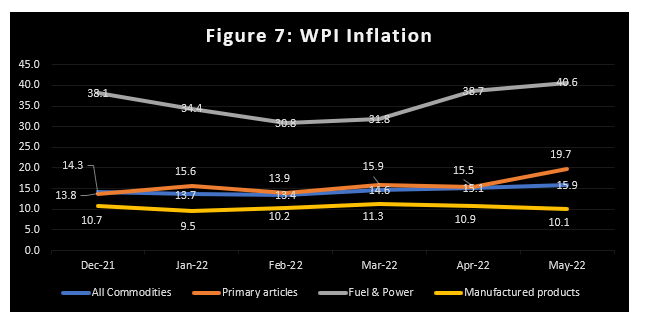

India’s wholesale price index (WPI) inflation increased from 15.1 in April to 15.9% in May, the highest level since August 1991, driven by soaring inflation of primary articles (15.5% to 19.7%) and fuel and power inflation (38.7% to 40.6%) (Figure 7). The wholesale inflation of manufactured products, however, eased from 10.9% to 10.1% (Figure 7).

Figure 8 shows that, the gap between wholesale and retail inflation narrowed down from 8.61% in December 2021 to 7.29% in April 2022, before rising to 8.84% in May. This was when retail inflation eased from 7.8% to 7% and wholesale inflation surged from 15.1% to 15.9%.

WPI inflation in the country has been increasing much faster than CPI inflation, since March 2021. Consequently, it is expected that retail inflation would slowly move closer towards wholesale inflation, in the months to come. Dr. Pronab Sen, former Chief Statistician of India has put it succinctly: “Rising WPI will, by and large, translate into higher retail prices.” High wholesale inflation indicates that input price pressures are still quite high, which will eventually reflect on retail prices.

Addressing Inflationary Woes

The RBI raised the policy repo rate by 40 bps in May 2022 and 50 bps in June 2022. The central bank is no longer behind the curve and the transmission of the rate in the banking system is also expected to be reasonably quick. While increasing the repo rate could hurt India’s economic recovery, the inability to control inflation will hurt the country’s growth prospects in the medium to long term.

RBI’s inflation projection for FY23 is 6.7%. It is expected that RBI’s Monetary Policy Committee (MPC) could raise the policy repo rate by 60-85 bps by December 2023, i.e., to 5.5-5.75%, depending on the inflation trajectory. A further cause for concern is the depreciation of the rupee, which could worsen inflation. RBI Governor Mr. Shaktikanta Das, in his June 08, 2022 statement on the Monetary Policy has expressed RBI’s approach to control inflation as: “Our approach underscores a commitment to move towards normal monetary conditions in a calibrated manner. We will remain focused on bringing down inflation closer to the target and fostering macroeconomic stability.”

The full impact of the measures announced by the government, viz, excise duty cuts on petrol and diesel, could be seen in the June inflation figure, as the cut in excise duty was announced in the last week of May. With the end of Russia-Ukraine conflict nowhere in sight, inflationary situation could worsen across the world. Although there has been a steady rise in revenue collection so far in FY23, GoI may have to tread the tightrope of balancing excise duty cut for controlling fuel inflation with incurring the budgeted capital expenditure for economic growth.